A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

What the Venezuela Tanker Seizure Signals 🇻🇪 Scrap The Cap 🛢️ The Lessons of China’s First-Ever Trillion-Dollar Trade Surplus 🇨🇳

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️Dry 🚢

Other 🌎

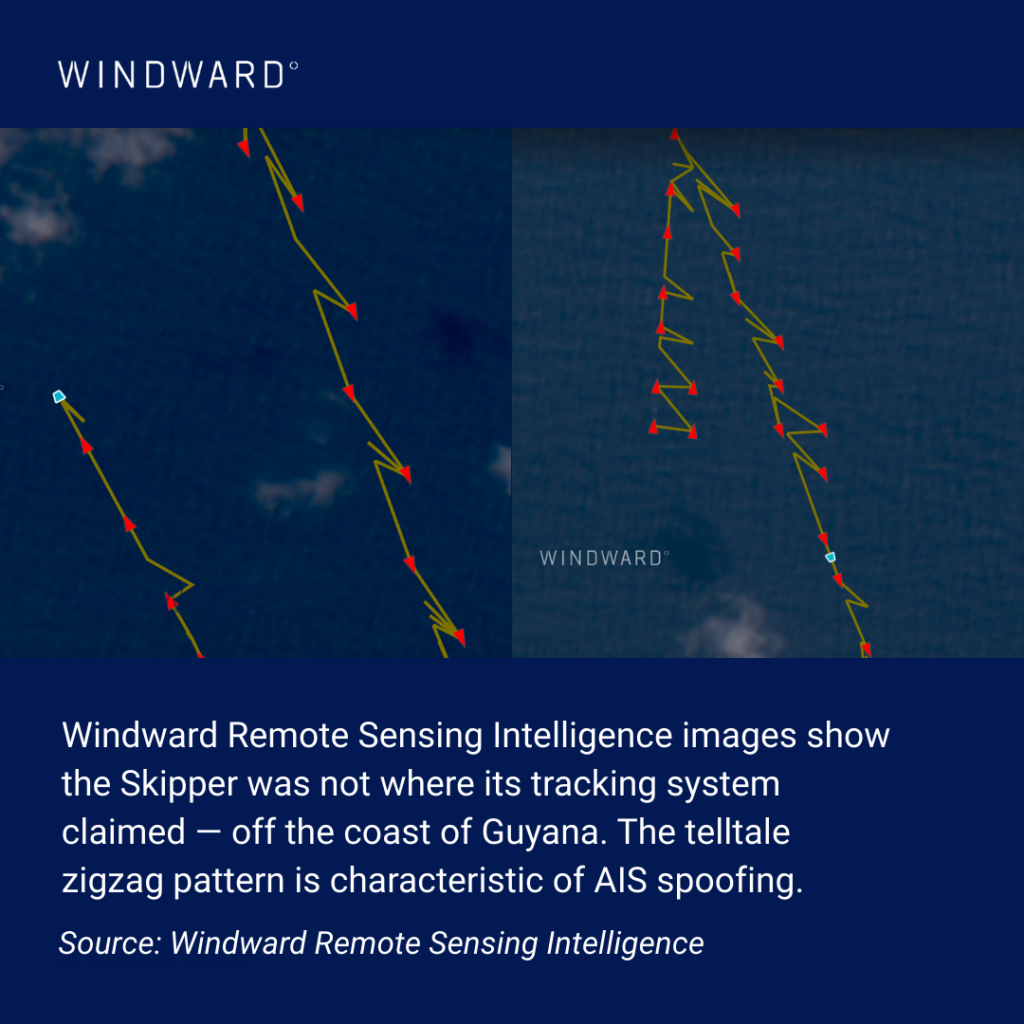

What the Venezuela Tanker Seizure Signals - WindwardSkipper was not an outlier. It represented the dominant operating model of today’s dark fleet. Sanctioned in 2022 for its role in an oil-smuggling network tied to Iran and Hezbollah, the vessel continued operating by exploiting systemic weaknesses. It broadcast AIS data that later proved inconsistent with its true movements. At the time of the boarding, Skipper’s AIS placed the tanker more than 500 nautical miles away, off the coast of Guyana. Windward’s Remote Sensing Intelligence showed otherwise. Satellite-based detections confirmed the vessel was nowhere near its declared position and had been conducting GNSS manipulation since October 28, broadcasting false coordinates while covertly loading sanctioned crude at Venezuela’s José terminal.

Its position reappeared more than 360 nautical miles from its last spoofed signal. It sailed under the flag of Guyana, a registry that has not existed since 2021, rendering the vessel effectively stateless.

This combination – sanctions exposure, AIS manipulation, and false flagging – is now common. Roughly 400 tankers are currently broadcasting affiliation with fraudulent registries listed by the International Maritime Organization, with nearly 300 already sanctioned. Together, they form part of a broader dark fleet of around 1,000 tankers transporting sanctioned oil for Russia, Iran, and Venezuela. What distinguishes Skipper is not its behavior, but the response it triggered. What Has Changed in Enforcement PostureThe seizure of Skipper reflects a more direct application of existing sanctions authorities rather than a new legal framework. The day after the seizure, the United States sanctioned six shipowners whose VLCCs had been transporting Venezuelan crude. According to the U.S. Treasury, four of those vessels manipulated AIS to conceal port calls and vessel movements. These practices were already well documented. What changed was how that information was acted upon. In Skipper’s case, the vessel was sanctioned, falsely flagged, and effectively stateless. Those conditions removed many of the protections that dark fleet operators have historically relied on to continue trading despite enforcement pressure. The seizure did not require a military escalation or a new sanctions regime. It relied on existing legal authorities applied decisively. This signals a narrower but more consequential shift: when sanctions violations, AIS manipulation, and false flagging converge, enforcement may no longer stop at designation alone. Physical intervention has become a viable outcome under specific, documentable conditions.

Scrap The Cap - GibsonsScrap the CapLast week news broke that the G7 group of countries were considering removing the oil price cap, which was first implemented at the end of 2022 following Russia’s invasion of Ukraine. The removal of the cap would see a full and unconditional ban on G7/EU companies providing maritime services to support Russian oil trade, in effect pushing Russian business entirely to the shadow fleet. Whether this is bullish or bearish for tankers depends on a number of key factors. It is understood that the British, European, and even American officials are promoting the idea. Even without US involvement, a full maritime services ban could force almost all mainstream tanker owners from the Russian market. Indeed, back in September, the UK and the EU lowered the price cap to $47.60/bbl. The US refrained from joining the lower cap, however, given the importance of London in maritime insurance and the fact that many of the major lifters of Russian price cap oil are located in the EU, the de facto price cap globally became $47.60/bbl instead of the G7 official $60/bbl. Something similar is likely to happen in the event of a full maritime services ban, with it being very difficult for any mainstream shipping player to circumvent EU or UK restrictions. As such, it may not matter whether the US joins or not. So, if a full maritime services ban is implemented, what might the impact be? Given the ban would force mainstream tanker owners to completely withdraw from Russian trade, one could argue that benchmark tanker rates could come under pressure given it would theoretically increase the number of tankers available for conventional trade. However, much would depend on how the buyers of Russian oil react. Generally, it is not considered a sanctions breach if a buyer uses non-sanctioned tankers and non-G7 services (finance, insurance brokerage, etc.) to transport Russian oil, regardless of the price paid. If Russia can access sufficient non-sanctioned tonnage and India and China remain major buyers of Russian oil, then the impact could be blunted. The timing of the implementation is also key. It is understood that the measures could form part of the EU’s 20th sanctions package due early in 2026, although some reports suggest the measures could be approved as soon as next week. What is not clear, is how long the phase out period might be. When the price cap was lowered in September, the UK gave a 6-week wind down period. If the implementation period this time is equally short, then it may be tough for Russia to adjust supply chains in time. However, if a longer wind down period is given, then Russia will have time to expand its fleet. This in turn would fuel the S&P market for older tonnage, boosting asset prices for older ships. The migration of older tankers from the mainstream to shadow fleet could also help offset any negative impact from tankers leaving Russian trade and returning to conventional markets. Overall, the measures are likely to shrink the addressable market for tanker owners who choose not to trade sanctioned cargoes. How negative that is, depends on whether this is balanced by the migration of ships to the shadow fleet. Likewise, if further sanctions pressure forces buyers of Russian crude to reduce their volumes, then we could see upside for mainstream tanker rates. Finally, all of this assumes a path to peace is not found, yet, with Trump pushing for peace by Christmas, some sort of deal cannot be ruled out either.

The Lessons of China’s First-Ever Trillion-Dollar Trade Surplus - Trade Data MonitorAfter falling year-on-year in October, China’s exports rebounded in November enough that it is almost certain that for 2025, the country that was mired in poverty when you and I were born will become the first nation ever to record a trillion-dollar trade surplus. The number is just a number, but it’s a big one, and it’s sending shockwaves through boardrooms and national leadership offices across the globe. French president Emmanuel Macron has warned that Europe may have to follow the U.S. in enacting protectionist measures. A Nice November (for China) For November, Chinese exports increased 5.9% year-on-year to $330.4 billion. That pushed up total exports for the year to $3.41 trillion. With overall imports at $2.34 trillion, the overall surplus sits at $1.07 trillion. It’s unlikely that China will run a trade deficit in December, meaning that the surplus will hold for full-year 2025. In 2024, China’s trade surplus came in just under a trillion dollars. Overall, imports rose 1.9% in November to $218.7 billon. Imports from the U.S. declined 19% to $10.1 billon. Imports from the EU ticked up 1.7% to $22 billion. Imports from Vietnam increased 9.8% to $8.8 billion.

How It Started How China got here is a well-chronicled tale. In the 1980s and 1990s, export-focused policies of communist party leadership and vast resources including a phenomenal domestic labor force and massive internal market attracted capital from across the globe and prompted allies to support China’s accession to the World Trade Organization in 2001. In this decade, there’s been a protectionist reaction led by the U.S. that has sought to dent Chinese exports. By some measures, it’s succeeded. Chinese exports in November to the U.S. dropped 28.5% year-on-year to $33.8 billion. For some products, China seems on its way out as the world’s dominant supplier. In November, exports of garments, footwear and toys all fell by over 10% year-on-year. Even shipments of mobile phones, a mainstay of the Chinese manufacturing miracle, dropped 12.5% to $14.8 billion. How It’s Going But what policymakers are now being forced to reckon with is that China’s export machine is so versatile and sprawling, with so many foreign markets, that it can easily adjust to the world’s largest economy trying to cut it off. As exports to the U.S. have slowed, those to Europe have rebounded in 2025. Shipments to the European Union increased 14.9% in November to $47.1 billion. Exports to ASEAN nations increased 8.4% to $58.1 billion. Sales to Vietnam jumped 25.8% to $18.3 billon. Exports to Africa increased 27.7% to $20.9 billion. China has also found new industries to dominate. Exports of motor vehicles in November rose 52.9% to $13.9 billion. Exports of ships increased 46.5% to $5.1 billion. As it’s built up its industrial manufacturing capacity, China has also been making its own market difficult to penetrate. Car imports dropped 41% in November to $1.9 billion. Sales of agricultural products rose 2.4% to $10 billion. Shipments of fertilizers increased 40.2% to $1.4 billion.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Import loss, stock build: How China absorbs the Hormuz shock (Link) From Supply Disruption to Transit Disruption: What April Reveals About the Global LNG Shock (Link) OFAC’s Crackdown on Chinese Teapot Refineries (Link) Dry 🚢 China’s soybean imports in March rose 14.9% (Link) Agri- Commodities: 27-01/05/26...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ The Clock is Ticking (Link) Asia crude slate shifts lighter as Middle East losses deepen (Link) Current Russian LNG Supply Picture (Link) Dry 🚢 Panamax Supply Outlook as Hormuz Faces Strain (Link) Dry Bulk Freight Recap: 17/04/2026 (Link) Other 🌎 Iran claims seizure of two MSC-operated boxships while...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Crude Tanker Activity Increases at Yanbu as Red Sea Export Flows Rise (Link) Asia crude slate shifts lighter as Middle East losses deepen (Link) Dry 🚢 China produced 160 million tonnes of crude steel in the first two months of 2026, down 3.6% (Link) Agricultural Commodities Overview - 03/26 (Link) Other 🌎...