A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

China’s soybean imports pivot south 🇨🇳 Why have most Iranian oil vessels turned their AIS signal back on? 🔎 Tit for Tat 🇺🇸🇨🇳

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

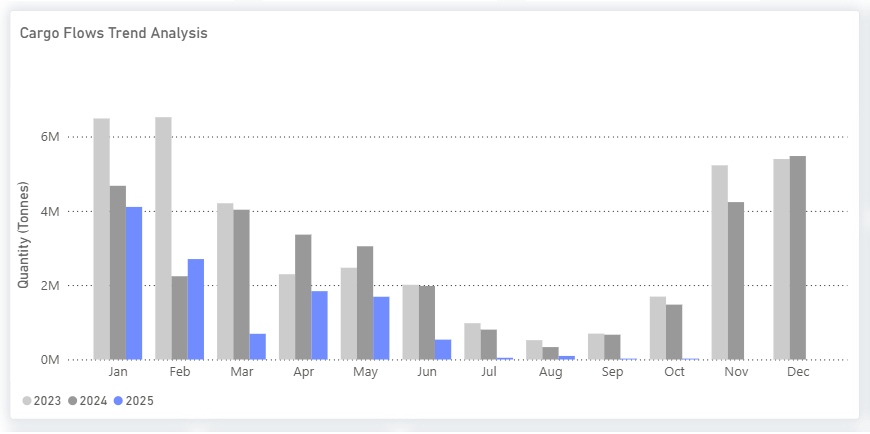

China’s soybean imports pivot south - Signal OceanU.S. shipments vanish in September as South America fills the gap China’s soybean supply chain took a sharp turn south in September.

U.S. cargo flows to China - collapse by September 2025 Shipments reached a peak of 4.1 Mt in January and decreased to 2.7 Mt in February, then fell to zero in September 2025; 2025 clearly differs from 2024, confirming customs reports of no U.S. soybean arrivals.

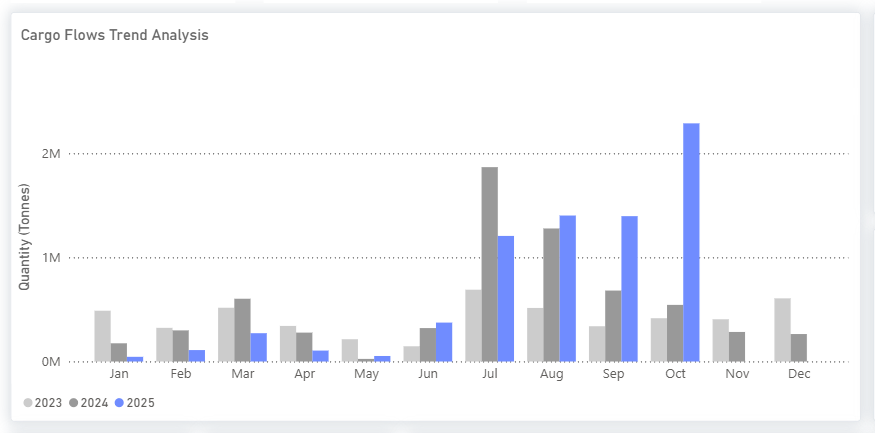

Argentina steps up - export incentives spark surge From August to October 2025, shipments experienced a significant increase. September saw nearly 1.5 Mt, approximately double the 2024 figures, largely due to temporary export-tax relief and a weakened peso, which enhanced export competitiveness. October volumes climbed even higher to about 2.3 Mt, marking a 64% month-on-month rise and over 320% year-on-year growth.

Brazil maintains dominance Sustained high volumes from April to August (10–11 Mt/month) and elevated September shipments versus previous years highlight Brazil’s extended export window and robust port capacity, though the 22.8% MoM decline in September reflects Argentina’s seasonal return to the export market.

Why have most Iranian oil vessels turned their AIS signal back on? - KplerIn a significant break from years of cloaked operations, Iranian crude tankers - including non-Iranian-flagged ships - are now transmitting AIS signals with rare consistency. Kpler’s latest tracking shows that only 14 out of 89 vessels carrying Iranian oil remained dark over the past 48 hours, reversing a longstanding evasion pattern. The timing of this shift is fuelling market speculation that sanctions relief is coming. It follows US President Donald Trump’s recent remarks in Israel’s Knesset, where he stated he would “love to remove sanctions when Iran is ready to talk.” While rhetorically notable, Kpler finds no current evidence of impending sanctions relief. Nuclear negotiations remain stalled over uranium enrichment levels, with the US maintaining its demand for zero enrichment — a condition Iran continues to reject. Direct backchannels may exist, but diplomacy remains gridlocked. Instead, a more credible driver may be Iran’s legal positioning under the UN snapback mechanism, which reinstated pre-2015 sanctions. These reimposed measures expand the legal basis for third countries to detain or seize Iranian tankers, especially those lacking proper insurance. By reactivating AIS signals, Iran may be seeking to demonstrate cargo legitimacy: showing that vessels are transporting crude, not prohibited goods such as arms or nuclear-related materials. Enhanced visibility could be a strategic effort to reduce seizure risk by signalling compliance with maritime norms under international law. Vessels shown loading from Kharg Island

This AIS shift could also serve as a strategic deterrent: making Iranian cargoes visible could signal that any seizure could be met with retaliatory action, particularly in the Strait of Hormuz, where Iran has previously targeted foreign tankers in tit-for-tat enforcement. While less likely, the move could also be intended as a display of resilience: a signal that US and UN sanctions are not disrupting the volume or consistency of crude exports to China, despite mounting legal and logistical pressure. A third, subtler angle lies with China. Iran may be using AIS transparency to build political goodwill with Beijing, which, alongside Russia, opposed the UN snapback. But the move also risks exposing China diplomatically. Despite its rejection of both US and UN sanctions, China generally masks Iranian imports under third-country origins (e.g. Malaysia). Open AIS tracking could complicate Beijing’s effort to maintain plausible deniability. Another possibility is that, following US sanctions on the Rizhao Terminal last week, China plans to no longer bow to US pressure and disregard sanctions. The US has increased pressure on vessels that handle Iranian crude this year. Over 60% of the vessels that have loaded Iranian crude in the last 12 months are now sanctioned by OFAC, having risen from 38% one year ago. This has ramifications on the whole logistics chain as most Chinese ports won’t receive vessels sanctioned by OFAC. As a result, more Iranian crude cargoes need to be transferred to a “clean” ship before discharge, increasing the cost. If there is a change in approach from China, and all ports are able to receive sanctioned vessels, there will be no need to hide vessel locations or move the cargo between sanctioned and non-sanctioned vessels, reducing logistical costs for Iran.

Tit for Tat - GibsonsOn October 14, both the US and China imposed prohibitively expensive port fees on tonnage linked to the other country. The USTR’s Section 301 measures were published and analysed well in advance. In contrast, China’s measures arrived with little notice; Beijing issued only a late-September warning that it would retaliate. China’s special port fees apply to any ship with clear US links calling at Chinese ports: vessels owned or operated by US companies or individuals; vessels owned or operated by entities in which US companies, organisations, or individuals directly or indirectly hold 25 percent or more of the equity (voting rights or board seats); US-flag vessels; and US-built vessels. There are two notable exceptions: first, vessels built in China are exempt; and second, ships arriving in ballast solely for repairs are also exempt. The fee levels are extreme – roughly $6 million per call for a VLCC and about $750,000 for an MR – clearly designed to have an impact. On the tanker side, US shipowners are few, and US-flagged or US-built deep-sea tonnage is insignificant. However, the US-operated fleet is sizable because oil majors and refiners typically maintain large time-chartered fleets. The real challenge lies in screening for the 25 percent US equity-control test. Many publicly listed owners have complex structures, and beneficial ownership can fluctuate over time. Several major non-US owners, particularly in Greece and Scandinavia, are listed on the NYSE or Nasdaq, further blurring the lines between “US-linked” and “international” for the purposes of the rule. When all US-listed companies are included, the portion of vessels captured by China’s fees rises. For tankers, it averages around 17% once China-built ships are excluded, though this varies by size class. It is worth stressing, however, that this figure remains a broad estimate. Some large US-listed owners, particularly those not based in the US, may fall below the 25% threshold and thus be exempt. Conversely, some companies with no obvious US ties may still have US equity stakes at or above 25%. VLCCs are the most exposed, as China is the single largest destination for this class, accounting for about 38% of VLCC trade on an export-volume basis last year. Other classes will also feel the impact, though to a considerably lesser extent, given their more diversified trading patterns and lower reliance on China. In the near term, the uncertainty over who is safe to trade into China could fuel additional freight volatility. The VLCC market is already very tight, supported by rising OPEC+ crude production, refinery maintenance, reduced direct crude burn for power generation in the Middle East, and a larger pull of Atlantic Basin crude eastward during September.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Crude Tanker Activity Increases at Yanbu as Red Sea Export Flows Rise (Link) Asia crude slate shifts lighter as Middle East losses deepen (Link) Dry 🚢 China produced 160 million tonnes of crude steel in the first two months of 2026, down 3.6% (Link) Agricultural Commodities Overview - 03/26 (Link) Other 🌎...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Upstream Under Attack (Link) Keeping Up With The Joneses (Act)(Link) The Strait of Hormuz remains constrained but operational under a clearly selective transit framework (Link) 'Zombie ship' uses fake ID to shuttle Iranian oil through Strait of Hormuz (Link) Dry 🚢 U.S. Overtakes Brazil in Corn Exports to...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Transit activity through the Strait of Hormuz remained heavily suppressed (Link) Middle East Mayhem (Link) Strait of Hormuz Disruption - Scenario Analysis (Link) Dry 🚢 Dry Bulk Impact of Trump's Spain Threat (Link) Agricultural Freight Overview (Link) Other 🌎 The Supreme Court’s IEEPA tariff decision: What...