A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Chinese Exports Down 1.1% in October 🇨🇳 Is the dirty tanker rally coming to an end? 🛢️ Sanctioned Russia-Trading Tankers Find Refuge in Duqm 🔦

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

Chinese Exports Down 1.1% in October - Trade Data MonitorThe Chinese export juggernaut finally started to show the impact of protectionism and weaker Western consumer markets in October. A week after Presidents Trump and Xi settled a new trade deal that cut tariffs and put off their trade war for a year, China reported a 1.1% year-on-year drop in exports to $305.3 billion. To be sure, this is only one month. China has shown resiliency thus far in 2025, finding other markets as Washington puts up obstacles to its exports. Shipments to the U.S. have declining since the spring. In October, exports to the U.S. fell 25.1% year-on-year to $34.9 billion. But sale to the European Union, especially Germany and France, had been holding steady. In October, surprisingly, they rose only 1%, to $43.9 billion. Analysts had predicted a 3% overall increase in exports, meaning that China missed its target by 4 percentage points.

Much of the recent analysis has focused on protectionist trade policies driven by populist politics. Although they have caused headaches for businesses by creating a climate of uncertainty, real tariffs have been lower than headline duties. Instead, a big part of the leveling off of Chinese exports has been caused by a change in its export composition, and in consumer demand in the U.S. and Europe. That’s why there’s been dramatic drops in shipments of consumer goods where China used to dominate. In October, for example, toy exports fell a whopping 31% to $2.5 billion. Shoe sales dropped 20.9% to $2.7 billion. Suitcase exports declined 25.7% to $2.1 billion. It’s not just the low-tech stuff. The number of mobile phones shipped dropped 14.2% to 70.6 million. Exports of high-tech products increased a modest 1.8% to $83 billion. Meanwhile, China is dominating new markets, especially in the automotive sector. Car shipments boomed again in October, rising 34.1% year-on-year to $14.3 billion. In Europe and the U.S., China still has to contend with strong domestic manufacturers. These exports tend to go elsewhere. China’s top 10 car markets so far this year: UAE, Russia, Belgium, UK, Mexico, Australia, Brazil, Saudi Arabia, Spain, Kazakhstan.

Is the dirty tanker rally coming to an end? - VortexaThe dirty tanker market continues to ride strong momentum, supported by a surge in oil on water, a divergence between laden and ballast speeds, and an uptick in long-haul voyages heading East. At the forefront of this strength are the VLCCs, which remain the clear leaders in the current market rally. VLCC utilisation now stands at around 57% — the highest level since 2020, when the price shock triggered a floating storage boom. Employment has been robust across both sanctioned and non-sanctioned grades, underscoring the market's buoyancy. Freight rates tell a similar story. VLCC rates are hovering near their strongest levels since 2020, though they have recently eased by about 20% from last week’s highs. Is this signaling the beginning of the end for the dirty tanker freight rate rally?

Vessel availability has tightened notably. The current build-up in oil on water and a series of discharge delays linked to new regulatory and sanction-related complications. From USTR and China’s Special Port fees to Rizhao and Yulong sanctions, the factors have all constrained available tonnage. That said, the direct impact of the latest sanctions on Russian entities will likely materialise following the 21st of November, extending voyage distances and keeping more dark fleet/sanctioned tonnage tied up. This is occurring at a point where increasingly more vessels are transitioning from the mainstream to the dark fleet — a move that is difficult to reverse and effectively reduces available tonnage for compliant trades. On the vessel demand side, buyers of Russian barrels are reportedly shifting towards mainstream grades, some of which involve long-haul trades from the Americas.

Together, these trends form a bullish backdrop for dirty freight. VLCCs and Suezmaxes are well-positioned to capitalize on longer-haul flows to India and China, while Aframaxes should also benefit from reduced competition, both from vessels moving into the dark fleet and from larger ships that captured a share of Atlantic trades earlier in 2025. Thus, short-term freight fundamentals seem to remain firmly on the bullish side.

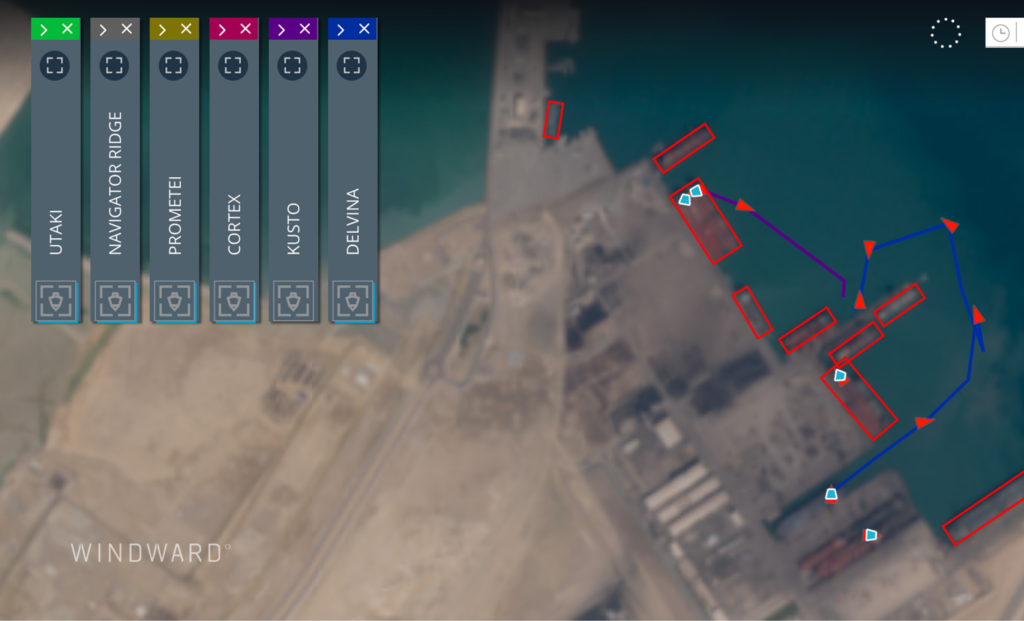

Sanctioned Russia-Trading Tankers Find Refuge in Duqm, Oman - WindwardSix sanctioned Russia-trading tankers are signaling that they are berthed at the Oman port of Duqm, amid an escalation in deceptive shipping practices in the area as key buyers in India and China pause or review oil purchases. The tankers, all part of Russia’s sanctions-evading shadow fleet, are broadcasting Automatic Identification System (AIS) signals placing them at berths in Duqm, with five arriving between October 27 and November 11. They are Utaki (IMO 9262924), Navigator Ridge (IMO 9321689), Prometei (IMO 9296597), Cortex (IMO 9291250), and Kusto (IMO 9308833). A sixth tanker, Delvina (IMO 9331153), signaled its arrival on September 24 and has broadcast AIS positions at various berths at the port since then.

Escalating Sanctions Pressure and Concealment TacticsUtaki, a 2002-built Aframax tanker formerly known as Linda and Bonnie, is flagged in Sierra Leone and is sanctioned by the UK and EU, but not the U.S. The tankers’ movements are yet another sign of the upheaval and disruption to Russian oil sales triggered by UK and U.S. sanctions imposed on Russia’s two largest oil producers, Rosneft and Lukoil, on October 15 and 22. Rosneft and Lukoil together account for more than half of Russia’s 3.5 million bpd of crude exports. Waters off Oman have long been used for covert ship-to-ship transfers of sanctioned oil, typically from Iran, but Russia’s use of the area was first observed in late 2024 and has continued into 2025. Tankers use GNSS manipulation, known as spoofing, in Omani waters to conceal STS activities. Russian oil is transferred onto so-called “clean” tankers that have not been sanctioned for onward shipment to ports in India and China, obscuring the origin of both the cargo and the vessel.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Crude Tanker Activity Increases at Yanbu as Red Sea Export Flows Rise (Link) Asia crude slate shifts lighter as Middle East losses deepen (Link) Dry 🚢 China produced 160 million tonnes of crude steel in the first two months of 2026, down 3.6% (Link) Agricultural Commodities Overview - 03/26 (Link) Other 🌎...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Upstream Under Attack (Link) Keeping Up With The Joneses (Act)(Link) The Strait of Hormuz remains constrained but operational under a clearly selective transit framework (Link) 'Zombie ship' uses fake ID to shuttle Iranian oil through Strait of Hormuz (Link) Dry 🚢 U.S. Overtakes Brazil in Corn Exports to...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Transit activity through the Strait of Hormuz remained heavily suppressed (Link) Middle East Mayhem (Link) Strait of Hormuz Disruption - Scenario Analysis (Link) Dry 🚢 Dry Bulk Impact of Trump's Spain Threat (Link) Agricultural Freight Overview (Link) Other 🌎 The Supreme Court’s IEEPA tariff decision: What...