A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Chinese Shipping In The Crosshairs 🇨🇳 Russia's Shadow Fleet Has Been Busy 🔎 Dry bulk freight earnings gain on iron ore congestion and Pacific coal chartering 🚢

|

Maritimedata.ai is a digital broker of data and analytics solutions for the maritime ecosystem. Source, Evaluate and Purchase maritime data and analytics from the largest network of specialised providers in the world. 200+ Products 50+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Explore, test, and feedback on maritime data solutions before they hit the market.We're delighted to be launching a number of beta tests for new-to-market data services over the next few months, and we'd like to offer you the opportunity to take part. Upcoming Opportunities 2025

How to get involved?You can register your interest for future beta tests below.

Chinese Shipping In The Crosshairs - Poten & PartnersAccording to the office of the U.S. Trade Representative (USTR), China is targeting the maritime, logistics and shipbuilding sectors for dominance. The USTR concluded this at the tail end of the Biden Administration in response to a petition filed by five U.S. labor unions back in March 2024. Under Section 301 of the Trade Act of 1974, the USTR is allowed to “address unreasonable or discriminatory acts, policies or practices that burden or restrict U.S. commerce”. Now, the new Trump Administration has announced the actions it proposes to take. It is considering imposing additional fees on Chinese shipping companies, companies that use Chinese ships and/or companies that have ships on order in China each time one of their vessels enters a U.S. port. The USTR also proposed a requirement that a percentage of U.S. exports are transported on U.S.-flagged ships, a subset of which would also need to be U.S. built. At this point, this is only a proposal (the USTR is asking for public comments by 24 March 2025) and important details with respect to implementation & enforcement are still unclear. However, in this Tanker Opinion, we will try to determine how implementation of proposals as they are currently written, may impact the crude oil and product tanker market. The main elements of the proposals are as follows:

To determine what might happen to the tanker trades if these rules are being put into effect “as-is” later this year, we have to put things in perspective. Based on Vortexa data, tankers made an estimated 12,108 port calls in 2024 (Chart 1). We don’t know how many of these calls were made by Chinese operators or operators with Chinese built vessels in their fleet or operators with newbuildings on order at Chinese shipyards. However, if we take a look at the current tanker fleet and the orderbook, we can get a general feel for the numbers. As per February 1st, the total tanker fleet of vessels >10,000 dwt consists of some 6,907 ships, of which 1,548 (22%) are built in China. Out of the total orderbook of 1,130 tankers, 788 (70%!) are being built in China.

Russia's Shadow Fleet Has Been Busy - WindwardThis week marked the three-year anniversary of the Russian invasion of Ukraine (February 24, 2025). As we’ve discussed at length, the war has driven the emergence of Russia’s shadow fleet, or gray and dark fleets. They are used for smuggling Russian cargo while appearing legitimate, or at least trying to evade detection. As if commemorating its own anniversary, the shadow fleet has been exceptionally active these past few weeks. First-Time VisitsOver the recent 30-day period (January 25-February 24, 2025), 461 vessels flagged for sanctions compliance risk related to the Russian regime conducted 716 first-time visits to ports around the world. First-time visits are not inherently suspicious, but when occurring in bulk, specifically by vessels of interest that are related to sanctioned regimes, they could indicate:

This is why first-time visits in new geographies constitute an anomaly that is flagged in Windward’s platform, allowing users to scrutinize and monitor such events. A closer look at where these first visits occurred shows that the highest number was unexpectedly in Ukraine (30 visits), followed by Malaysia (25 visits). All of these vessels are affiliated with the Russian regime, either through ownership or behavioral indicators (port calls, for example). Several are also marked as high or moderate risk for smuggling. Among the higher-risk vessel groups, Malaysia emerged as the leading destination for first visits. As Western sanctions have tightened on its popular third-country allies, such as India and China, Russia has been seeking new markets and transit routes for its oil exports. Malaysia has clearly emerged as one of the new destinations for the shadow fleet. Malaysia’s position in Southeast Asia makes it an attractive transit point or destination for Russian oil exports, especially given the expanding Asian market for Russian oil. Unlike EU countries, Malaysia may have less rigorous enforcement of Western sanctions, making it a more accessible destination for the shadow fleet. Security Incidents Involving Russian Shadow Fleet TankersItalian port authorities reported an incident in the Savona port area buoy on February 14. Malta-flagged oil-product tanker Seajewel reported two explosions heard by the ship’s crew while offloading at one of the port’s offshore terminal buoys. Divers’ investigation of the Greek-owned vessel known to regularly trade Russian oil revealed two holes in the ship’s hull and dead fish around it. This raises the likelihood of an initiated explosion by an external factor. The vessel was transporting oil from Russia to Europe in violation of sanctions when these explosions occurred. Windward’s Maritime AI™ platform flagged the Seajewel as high risk for sanction compliance back in November 2024, based on its port calls in Russia, dark activity, and suspicious cargo. There was another suspicious explosion earlier this month, on February 9, in Ust Luga, Russia. It involved the Antigua and Barbuda-flagged crude oil tanker Koala, which was reportedly damaged by mines near the port. The Koala was flagged on February 4 by Windward as a moderate risk for smuggling, due to multiple and recent identity changes, irregular business structure, and dark activities, which is added to its sanctions compliance high-risk score, in part for being owned by a sanctioned company (Cyprus-based).

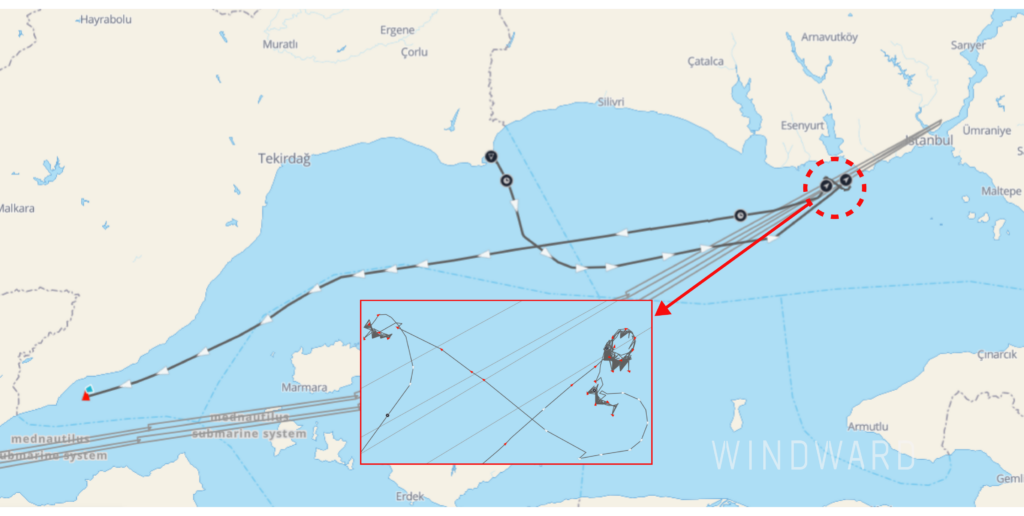

Suspicious Movements Around Turkish Underwater Cables There were reports in recent months that submarine cables were sabotaged in areas frequented by countries on either side of geopolitical divides – Russia and EU countries in the Baltic Sea, and China and Taiwan in the South China Sea. These events prompted probes into vessels that may be involved. Many of the vessels at the center of these investigations are shadow fleet ships. Windward analysts detected suspicious movements around the Mednautilus Submarine System infrastructure, located in the Sea of Marmara. A gray fleet vessel, sailing under the Panama flag and marked as a moderate smuggling risk and moderate compliance risk, displayed unusual behavior above the cable – including unusual loitering multiple times in February.

Dry bulk freight earnings gain on iron ore congestion and Pacific coal chartering - Kpler

|

|

Coal: Lower prices weigh on mining revenues, coal becomes competitive against petcoke

- Seaborne metallurgical coal deliveries rose by 500,000t w/w to 4.5 Mt last week, mainly driven by high demand from Japan and South Korea, while deliveries to India and China edged lower w/w.

- Seaborne thermal coal imports rebounded to 16.8 Mt last week from a low base of 13.7 Mt the previous week, driven by a recovery in receipts from China and India.

- The world’s largest thermal coal producer, Glencore, announced that it made a loss in 2024 owing to weaker coal prices and one-off impairment adjustments to its balance sheet. The company ruled out any immediate production cuts to its thermal and metallurgical coal production. Glencore’s latest guidance suggests thermal coal production will remain steady at around 100Mt until 2028. Thermal coal production is projected to fall after 2028 however, the company has not ruled out cutting output if market conditions deteriorate further. The company plans to produce around 30-35 Mtpa of metallurgical coal in the coming years, which aligns with its previous production levels and output from its latest metallurgical coal acquisition EVR’s mining assets.

- Despite the recovery, China’s thermal coal receipts are on track to fall for the second consecutive month. Kpler data indicates aggregate receipts will be around 20-21 Mt, down from 23 Mt last year. Mining operations in China have restarted after the end of the spring festival, which should weigh on the need for imports, given that early indicators suggest that coal consumption from the power sector is lower than 2024 levels so far this year. Chinese metallurgical coal demand also faces headings. However, this is unlikely to have a significant impact on the seaborne market given Mongolia’s role as a supplier to China via rail route. Metallurgical coal stocks at the Ganqumaodu crossing are growing at a steep rate due to weak offtake.

- Indian buyers also increased their thermal coal intake last week, with receipts from Indonesia, South Africa and the US gaining by 300-500,000t w/w to take aggregate receipts to 3.5Mt. The increase in US receipts coincides with petcoke’s eroding competitiveness into the country, as some traders are offering distressed Northern Appalachian coal cargoes into India at lower rates than petcoke on an energy-adjusted basis. Imports from the US rose to 400,000t last week, the highest since late May 2024.

India thermal coal imports from US (Mt)

|

| Read the full article here |

How we can help:

- Submit your requirement - A member of the team will reach out within 24 hours

- Book a call with the team - Explore which of our 200+ data and analytics solutions align with your needs

Thank you for your time.

Regards,

James Littlejohn

Co-Founder

Info@maritimedata.ai

You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe.

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single point of access to 200+ data services We integrate the best maritime data sources into custom data pipelines so you can focus on decisions, not discovery. 200+ Products 55+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Venezuela shock: Chevron exit to reshape heavy sour markets - (Link) The US & Iran - Deal or No Deal? (Link) Asian demand slump pushes fuels trans-Pacific (Link) Dry 🚢 Panamax Dry Bulk Market:...

Maritimedata.ai is a single point of access to 200+ data services We integrate the best maritime data sources into custom data pipelines so you can focus on decisions, not discovery. 200+ Products 55+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Opec Adds Fuel to the Fire - (Link) Oil flows from Saudi Arabia to China declined sharply (Link) Venezuelan crude exports drop in April amid export licence revocation (Link) Dry 🚢 Brazil...

Maritimedata.ai is an integrator and broker of data and analytics solutions for the maritime ecosystem. Source, Evaluate and Purchase maritime data and analytics from the largest network of specialised providers in the world. 200+ Products 50+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈 Oil & Gas 🛢️ Section 301 Saga - (Link) Make America Build Ships Again? (Link) USTR’s port fees have more bark than bite as exemptions minimise impact on oil/products fleet (Link) Dry 🚢...