A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Key US sectors at mercy of proposed 50% EU tariffs 🇺🇸 Red Sea traffic remains 60% lower than normal volumes 📉 Refinery Closures Are Accelerating 🛢️

|

Maritimedata.ai is a single point of access to 200+ data services We integrate the best maritime data sources into custom data pipelines so you can focus on decisions, not discovery. 200+ Products 55+ Maritime Intelligence Providers 30+ Years of Experience

Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

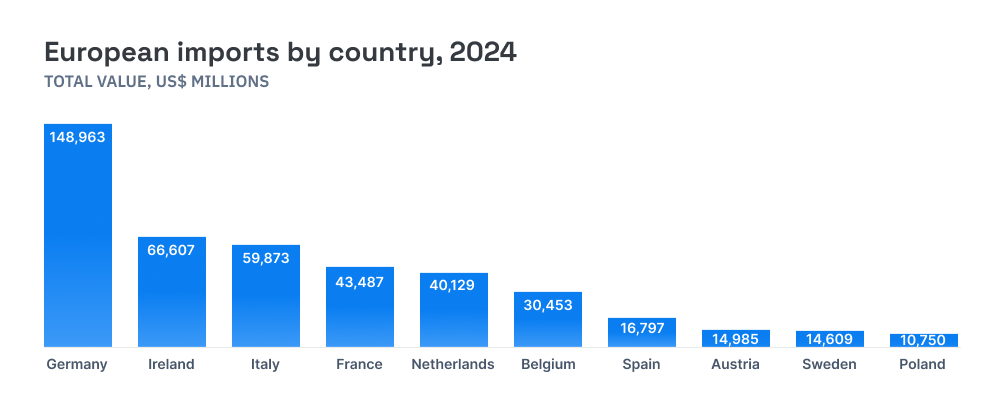

Key US sectors at mercy of proposed 50% EU tariffs - ImportGeniusFrom tiny pharmaceutical compounds to massive machinery, a trade war with Europe would send ripples throughout the United States economy. The spectre of a 50% tariff rate on all goods from the European Union has many sectors of the U.S. economy bracing for the impact of a new front in the global trade war. Last Friday afternoon, United States President Donald Trump, decrying the slow pace of trade negotiations with the EU, threatened to impose a 50% tariff on all imports from the 27-nation trading block in a matter of days, effective June 1. On Sunday President Trump softened his position, saying the 50% tariffs would come into effect on July 9 if a deal is not reached by then. While tariff announcements and trade wars have become routine since President Trump’s inauguration in January, the prospect of a trade war with Europe would be different. “Trade with Europe is a world apart from trade with China,” explains ImportGenius President Chris Schafer. “American imports from Europe tend to be higher-value items rather than inexpensive consumer products. But they are the kinds of high-value items that would impact the lives of nearly all Americans.” While the proposed 50% tariff would apply equally to every EU member state, each individual country has a different exposure to the U.S. market.

According to experts, a 50% tariff on EU imports — combined with EU counter-tariffs — could shrink the U.S. economy by 1.5%. Similar projections apply to numerous EU countries: 1.5% for Germany, 1.2% for Italy, 0.75% for France and 0.5% for Spain. But the hardest economic hit would be felt in Ireland, which relies heavily on pharmaceutical exports to the United States, and whose economy would contract by 4% as a result of the higher tariffs. European imports: top sectors and potential ripple effectsWith 27 member nations, the European Union is a diverse economy that provides the United States with a variety of high-value imports — and they’re not the goods you might expect. Only 5% of America’s EU imports in 2024 ($29.8 billion) were the often-mentioned, stereotypical “luxury” goods such as perfumes and makeup ($12.4 billion), precious gems ($9.4 billion), artwork and antiques ($5.5 billion), and leather handbags ($2.4 billion). By contrast, data from the US Trade Census analyzed by ImportGenius shows trade with the EU supports America’s health and medical sectors, accounting for more than one-third of its $605 billion in 2024 EU imports. The largest single category, accounting for 21% of European imports ($127 billion), is pharmaceutical products, whether over-the-counter or prescription medication. Some 6% of imports ($35.1 billion) fall under the category of organic chemicals. The lion’s share of this total ($15.6 billion) was semaglutide compounds, the key ingredient in many weight-loss medications. Another 6% of imports ($37 billion) are surgical and medical instruments, including hearing aids ($1.3 billion alone) and artificial joints such as knee and hip replacements ($2.5 billion). It remains to be seen whether any eventual trade deal with the EU will include some form of exemption for these products.

America also relies upon Europe’s advanced manufacturing and engineering industries, with another one-third of total imports coming from that sector. Machinery and mechanical parts accounted for 15% of European imports ($89.8 billion). This includes excavators and other large industrial equipment, impacting the U.S. based industries that rely on such machines. Vehicles made up 10% of imports ($60.3 billion), $23.4 billion of which were vehicles with 1.5 litre to 3.0 litre engines (100 to 200 horsepower). Electrical machinery and parts accounted for another 6% of the total ($39.2 billion). A total of $14.3 billion (2.5%) were imports of aircraft, spacecraft, and parts. The last item on that list, while fairly small, is significant because it’s part of the renewal and maintenance of America’s fleet of commercial aircraft — meaning that a 50% tariff could trickle down to the cost of airfare.

Red Sea traffic remains 60% lower than normal volumes - Lloyd's ListTraffic through the Red Sea chokepoints remains a far cry from normal levels, with last month’s US-Houthi ceasefire doing little to encourage owners and operators that have rerouted to resume transits. In May, there were 971 passings of cargo-carrying vessels of more than 10,000 dwt — those most likely to be internationally trading — through the Bab el Mandeb, according to Lloyd’s List Intelligence data. This is equivalent to 65.5m dwt. There were 891 transits through the Suez Canal last month, or 67.9m dwt in tonnage terms. These transit volumes are within the “new normal” range and 60% lower than pre-Houthi attack levels. That is not to say there has been no return to the beleaguered shipping lane over the past several months. Owners and operators started reviewing their stance on Bab el Mandeb transits after the now defunct ceasefire agreement between Israel and Hamas was implemented in January. This includes large companies that had been diverting from the area since the start of the crisis. Egypt has been trying to persuade shipping lines that have been reluctant to restart Red Sea voyages that safe navigation through the Red Sea is possible and, in a bid to boost traffic, the Suez Canal Authority is offering a 15% discount in transit fees for containerships.

Refinery Closures Are Accelerating - GibsonsTotal global refining capacity has been in an upwards trend for a long time, and years with declines are rare, barring those caused by overarching events such as the COVID pandemic. It is possible that this trend will soon change. Refinery closures are accelerating in the Atlantic Basin, driven by lower margins largely caused by structural demand developments. In recent months, global refining margins have been surprisingly strong, though maintenance activity and the closure of refineries are partly responsible. East of Suez, refining capacity is still growing, though at a slower pace than in previous years, whilst some capacity rationalisation is also prevalent in China. So far this year, the 260 kbd LyondellBasell refinery basin in Houston and Grangemouth (150 kbd) have shut their doors, and Wesseling (150 kbd), and Philips 66 Los Angeles (139 kbd) are scheduled to fully close or be repurposed. BP Gelsenkirchen is to close a third of its 257 kbd refinery and put the rest up for sale. Combined, these closures amount to around 800 kbd of capacity scheduled to shutter in the West this year. Closures may provide support to the margins of the remaining refineries, possibly helping to delay further shutdowns. However, European refining is likely to remain under pressure with Dangote expected to reach full scale gasoline production later in Q4, and demand also pressured in the key US export market. Given the competitive challenges facing European and some US refiners, even with the additions of Dangote and Olmeca, the IEA expects capacity in the Atlantic Basin to shrink faster than demand this year. The start-up of the 340 kbd Olmeca refinery has been beset by delays, and it is now expected to ramp up later in the year, though the timeline until full capacity is reached is unclear. Greater refining capacity in Mexico may push more US barrels into Europe to compensate for the loss of the Mexican export market, but the closure of Lyondell somewhat balances this. Globally, refinery capacity additions are largely taking place East of Suez, with additions in China, the Middle East, and India this year. In the Far East, some Chinese independent refiners have struggled to remain competitive and have been forced to close or cut runs, as increased difficulty in accessing cheap oil from Iran and Venezuela, and a push by Chinese policy makers to raise import taxes and limit rebates on fuel oil has weighed on margins. China has also been consolidating its state-owned refineries, with the 410 kbd Dalian refinery to be permanently shut from the end of this month. 2026 will see further refinery additions in the East, but there are no large-scale projects in the pipeline in Western economies. Beyond next year, the pipeline of new refinery capacity additions looks limited, though FIDs may still be taken. It is difficult to project what this all might mean for the clean tanker market. With demand in the largest markets in the West shrinking, clean tankers may find themselves turning East for employment. However, a significant share of new expansions East of Suez are focused on meeting domestic demand rather than export markets and may not benefit clean tankers. Some continued demand growth such as in Latin America may provide limited support, though in West Africa this could be met to a significant extent by increased local refining capacity provided by Dangote and other smaller local refineries. Additionally, if demand in especially Europe shrinks more slowly than refining capacity, we could see increased need for imports from East of Suez, possibly supporting clean tanker demand. Overall, the clean tanker market may no longer be able to rely on the long-standing upwards trend in global refining capacity, with new investments mostly taking place East of Suez, where demand is expected to continue to grow.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ What will crude oil overproduction do to tanker rates? (Link) Regulatory disruptions and oversupply support crude freight (Link) Tanker Market Tightens on MEG Liftings, OSP Cuts, and China Port Fees (Link) Dry 🚢 Weekly Freight Recap: 23/10/25 (Link) China’s soybean imports in September totalled 12.87 million...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Kurdish Crude Recommences (Link) More Barrels To The Med (Link) Russian gasoline exports dry up (Link) Dry 🚢 European Commission set out in early October a draft proposal to replace the bloc’s current steel safeguard system. (Link) Dry Bulk Freight Recap (Link) Minor bulk exports stay strong, but new...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Assessing the impact on Russian energy infrastructure from renewed Ukrainian drone strikes (Link) VLCCs Are Booming Again (Link) Reality check: China’s appetite for a new stockpiling wave (Link) Dry 🚢 Argentina temporarily eliminated export taxes on grains (Link) Agricultural Commodities Pricing Updates...