A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Advanced spoofing hides Russian oil transfers in Gulf of Oman 🔦 Key Dry Bulk Data Trends: August 2025 🌾 Moving metal: navigating costs, congestion, and carbon in the aluminium supply chain 🚢

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎London International Shipping weekWe're looking forward to the best minds in shipping descending upon London in mid-September. We'll be attending: 15/09: Lloyd's List Intelligence: Navigating Risk in an Uncertain Shipping Industry 16/09: WTW: Geopolitics in Shipping 16/09: Blue Communications: Video Killed the Radio Star 17/09: Windward: From Policy to Practice - Navigating maritime operations in 2025 17/09: SPNL: Evening Gala 18/09: North Standard: Breakfast Panel 18/09: Vortexa: Innovation Series 18/09: LISW25: Champagne Reception, Gala Dinner and After Party If you'd like to book a meeting with us while you're here please do so, or feel free to reach out if you plan to attend any of these events and would like to catch up. Advanced spoofing hides Russian oil transfers in Gulf of Oman - Lloyd's ListRUSSIA’S shadow fleet tankers are using sophisticated spoofing methods to disguise ship-to-ship transfers in the Gulf of Oman to circumvent sanctions and avoid detection by watchful regulators. Analysts at energy intelligence provider Vortexa first spotted the transhipment of Russian oil in this area in February 2024. At the time it was an infrequent occurrence, but this activity is on the rise and becoming more difficult to spot as tankers manipulate their positional data in increasingly sophisticated ways to avoid detection. Vortexa senior freight analyst Mary Melton said STS transfers in the Gulf of Oman enabled the transfer of Russian crude from a US Office of Foreign Assets Control-designated tanker to a non-Ofac-sanctioned tanker, which could then deliver the cargo to India or China. “Logistically, it also enables the sanctioned tankers to conduct the STS in a location further away from the ultimate discharge port and head back to Russia to load more quickly,” Melton said. Aframax Rozmarine (IMO: 9250531), for example, departed the port of Murmansk on January 28, two weeks after it was sanctioned by Ofac, laden with 738,000 barrels of Novy Port crude. It entered the Gulf of Aden on February 18 and started manipulating its positional information within days. At this point the Automatic Identification System trace, which showed the vessel taking a seemingly normal route up to the Gulf of Oman before turning back, is falsified. Rozmarine conducted a STS transfer with Sierra Leone-flagged Prisma (IMO: 9299678) during this period, according to Vortexa. Prisma also spoofed its location at this time, showing itself as manoeuvring off the southern coast of Oman, near Duqm. The cargo was delivered by Prisma to Lanshan, China at the end of March.

Key Dry Bulk Data Trends: August 2025 - AXSMarineThe Dry Bulk shipping market in August 2025 continued navigating a year of record highs, subtle declines, and fleet optimization challenges. By analyzing AIS-derived vessel tracking data enriched with commercial datasets, we uncover key trends in commodity flows, fleet utilization, and regional demand shaping the industry today. Fertilizer Imports Surge to Record LevelsGlobal fertilizer shipments reached nearly 120 million metric tons (MT) by July 2025, a 7.2% year-over-year increase. Brazil is the world’s largest importer, discharging over 24.5m MT—the highest ever recorded for this period—representing 20.9% of global seaborne fertilizer shipments. Key imported commodities include muriate of potash, ammonium sulphate, urea, and mono-ammonium phosphate.

India follows with 15.4m MT (+17.9% YoY), accounting for 13.1% of the global market. Its imports mainly comprise phosphate rock, urea, and di-ammonium phosphate. The United States places third so far in 2025, with 8.3m MT (-8.6% YoY), representing a 7% share. Indonesia increased fertilizer imports by 14.7% YoY (around 5.5m MT), while Australia remained stable at 5.1m MT. Iron Ore Shipping: Declines and Regional ShiftsIron ore shipping in 2025 is shaped by a size effect, with larger vessels maintaining steady volumes while smaller bulk carriers face declining utilization. These patterns underscore the importance of fleet optimization in a shifting global iron ore market. Global seaborne iron ore shipments exceeded 1 billion MT in August 2025, yet overall volumes are down 2.6% YoY. Most months from January to July recorded declines, with February dropping 13% YoY.

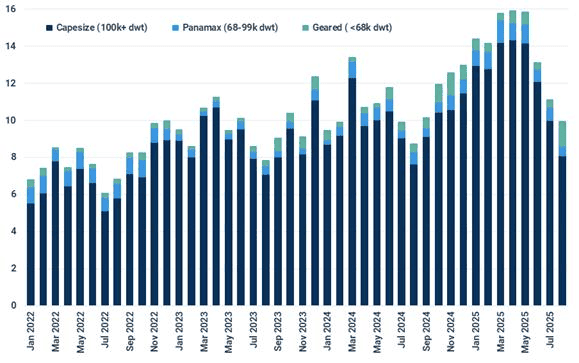

Moving metal: navigating costs, congestion, and carbon in the aluminium supply chain - KplerThe aluminium supply chain uses both dry bulk carriers and containership freight to move raw materials and products from producer to consumer. This leaves it open to two, sometimes divergent, sets of freight market fundamentals.Dry bulk carriers are employed to ship bauxite from mines to refineries, as well as alumina for further processing. Aluminium products are generally carried on containerships, although the high cost of container freight has occasionally pushed them onto small dry bulk carriers. There has been a divergence in the dry bulk freight market this year, with larger Capesize (100k+ dwt) vessels outperforming the smaller ships. Capesizes have enjoyed an average earnings premium of +32% to the smaller Panamax (68,000-99,999 dwt) in the year-to-date. This compares with a long-term average of only +12%. Alongside iron ore, Guinean bauxite exports to China are a key driver of Capesize market strength, with shipments up by 36% y/y to 96.90 Mt over January-August. Volumes are about to start ramping up again following a lull during the rainy season (May-October), and a strong pace of trade is expected, despite policy-driven uncertainty in the Guinean mining sector. By contrast, lower Pacific coal trade has weighed on earnings for sub-Capesize vessels. Guinean bauxite trade is dominated by Capesize cargoes to China (Mt)

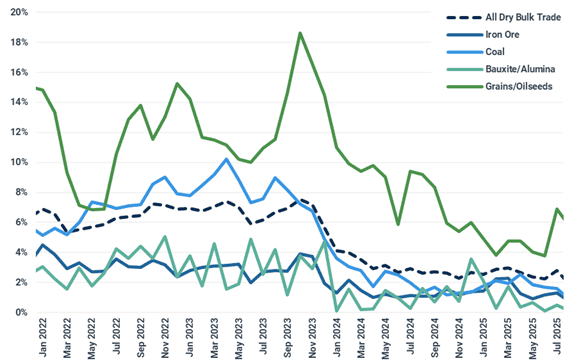

The containership market has been shaken by macro trends linked to trade tariffs and threats to global economic prosperity. Efforts by shippers to front-run tariffs generated volatility and market spikes, although overall earnings are still lagging behind 2024. The FBX Global Container Index is down by 27% y/y in 2025 to date. Containership earnings would be lower still were it not for the tightening effect on tonnage supply of vessels being forced to reroute around the Cape of Good Hope instead of sailing through the Red Sea. The sinking of two dry bulk carriers (Magic Seas and Eternity C) in July, plus subsequent attacks on shipping, have reinforced the risks of this route. Rerouting imposes additional costs on charterers with a Shanghai-Rotterdam voyage using the Cape of Good Hope, 30% longer and an extra eight days voyage time (at 17 knots) compared with the Red Sea route, with a consequent increase in carbon emissions. Without the supply-tightening effect of the Red Sea crisis, the surge in containership deliveries in 2024, when a massive 430 ships totalling 2.87 million TEU of capacity were delivered, would have resulted in lower costs for charterers and reduced earnings for owners. Dry bulk carriers are more willing to run the Red Sea risk. We have observed an upturn in dry cargo volume through the region since the start of the Russian Black Sea wheat export season. These are primarily cargoes for countries in the Middle East and East Africa, and sailing around the Cape of Good Hope would not be economical. We do not expect a normalisation of trade through the Red Sea in the short or medium term. Seaborne dry bulk trade via Red Sea/Suez Canal: upturn in grain shipments (% total trade)

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Transit activity through the Strait of Hormuz remained heavily suppressed (Link) Middle East Mayhem (Link) Strait of Hormuz Disruption - Scenario Analysis (Link) Dry 🚢 Dry Bulk Impact of Trump's Spain Threat (Link) Agricultural Freight Overview (Link) Other 🌎 The Supreme Court’s IEEPA tariff decision: What...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Russian Diesel Tanker Sails for Cuba as U.S. Order Blocks Oil Imports (Link) Does The Buy And Hold Strategy Still Work? (Link) Alaska Crude Diverts to Asian Markets (Link) Dry 🚢 A Market Increasingly Driven by Minerals Rather Than Energy (Link) Agricultural Freight Overview (Link) Other 🌎 Can Project Vault...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Reassessing Russian Supply (Link) Mainstream oil supplies return to normalcy as surplus falls (Link) Moscow, we have a problem (Link) Dry 🚢 Bauxite offers real positivity for capesizes (Link) Agricultural Freight Overview (Link) Copper Insights: The Supply-Demand Disconnect (Link) Other 🌎 How accurate were...