A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

India Crude Imports To Rebound In September And October 🛢️ New GPS Jamming Hotspot Seen at Third Russian Oil Export Port 💻The Future of Guinea's Position in Global Bauxite Trade And Its Alumina Ambition🇬🇳

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

London International Shipping weekWe're looking forward to the best minds in shipping descending upon London in mid-September. We'll be sharing the events we'll be attending, and hope to see many of you there. If you'd like to book a meeting with us while you're here please do so. India crude imports to rebound in September and October - VortexaIndia crude imports fall in August due to lower arrivals into Nayara Energy refinery. We expect crude flows into India to rise in September and October. India's crude imports are projected to fall by 0.3mbd m-o-m to 4.3mbd in August. Based on 9-year seasonal trends, arrivals of crude into India are typically the lowest in August. Domestic demand for gasoline and diesel used in road transport and agriculture decreases amid the monsoon season which begins in June and peaks in July-August. As such, most refineries conduct planned maintenance and reduce crude throughput during this period.

The reason behind this year's decline is different. India's lower crude imports this month were mainly due to the decrease in flows into Nayara Energy's refinery. Analysing crude arrivals into India by port, it is evident that the major decline in arrivals occurred at Vadinar, where Nayara Energy's refinery oil terminals are located. In fact, crude imports into Vadinar have fallen steadily for two consecutive months since July.

Focusing on Vadinar port and selecting oil terminals linked to Nayara Energy, we see that crude arrivals into the refinery fell by 0.1mbd m-o-m in August. Imports of non-Russian crude completely ceased this month as mainstream vessels avoid calling at Nayara Energy refinery terminal. Meanwhile, imports of Urals crude into the refinery have risen slightly this month, as vessels plying the Russia-India trade route resume crude discharges after brief disruptions last month. The overall drop in crude inflows impacted the refinery’s processing rates, resulting in a corresponding decrease in product exports. With the EU sanctions on Nayara Energy, the refinery will likely increase purchases of Russian crude in replacement of non-Russian barrels. Hence, we could see arrivals of crude into the refinery to rebound from August levels in the months ahead.

New GPS Jamming Hotspot Seen at Third Russian Oil Export Port - WindwardWindward has detected extensive GPS jamming in a new location at the eastern Russian port of Nakhodka, leading to a 30% rise in deliberate interference to ships’ navigation signals across the region over August. Between August 5-18 the Automatic Identification Signals (AIS) of 112 ships were transmitted on land at Nadhodkta port, the first time GPS jamming was noted in this area. The GPS jamming occurred across the bay from the Transneft export terminal at Kozmino, where crude is exported from the Eastern Siberia Pacific Ocean (ESPO) pipeline. This marks the third major Russian oil hub to be hit by deliberate signal interference, with similar GPS jamming disruptions noted for protracted periods in the Baltic Sea around Ust Luga and Primorisk, as well as Novorossiysk in the Black Sea.

Significant interference with tanker AIS signals linked to GNSS manipulation was already seen around Kozmino before GPS jamming was detected at Nadhokta. GPS jamming, which blocks ships’ AIS satellite signals, is a common tactic attributed to greyzone aggression to obscure maritime activity but is also a significant navigation hazard.

The tactic is different to GNSS manipulation, also known as spoofing, in which ships falsify their real AIS location in order to obfuscate their position. However both GPS jamming and GNSS manipulation add to difficulties tracking loading of oil by Russia-trading tankers.

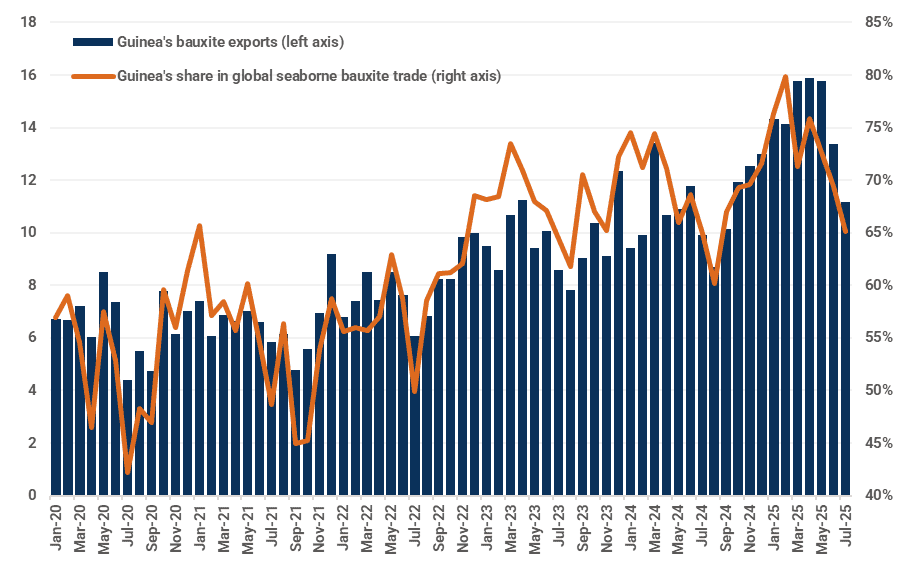

The future of Guinea's position in global bauxite trade and its alumina ambition - KplerIn the first seven months of 2025, Guinea accounted for 73% of global seaborne bauxite exports, consolidating its position as the dominant force in international bauxite trade. However, we have identified some headwinds that might shake Guinea's supremacy and hamper the country's ambition to build bauxite refining capacity.

Guinean bauxite exports and its share in global seaborne trade (Mt, %)

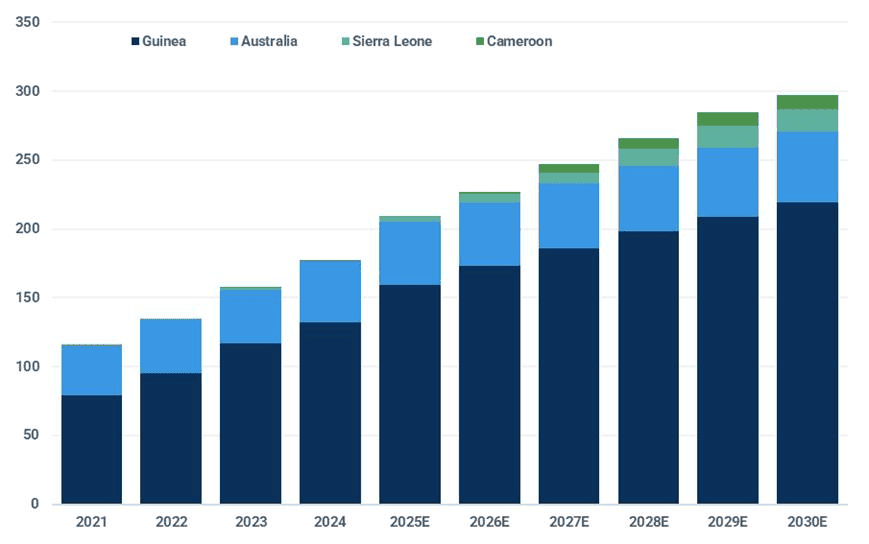

Will new capacity outside Guinea shake the country's dominant position in the bauxite trade?In Australia, sustained investment in production capacity and plateauing domestic demand will drive modest growth in bauxite exports in the coming years. Rio Tinto commenced work on the Norman Creek access project at the Amrun bauxite mine on Cape York Peninsula in Q3 2025, an integral component of the broader Weipa operation expansion. Concurrently, early works and a definitive feasibility study have commenced for the Kangwinan project, which is intended to replace the retiring Gove and Andoom mines. These initiatives could raise Rio Tinto's output in Australia by at least 7 Mtpa and reinforce long-term production stability. Metro Mining, the second-largest bauxite producer in Australia, could increase its annual shipment capacity from the current 6.50-7 Mtpa to 8 Mtpa, contingent upon the alleviation of barging bottlenecks and the successful execution of its expansion strategy. Collectively, these developments may lift the Australian bauxite exports to above the 50 Mtpa mark by the end of this decade and consolidate its position as the world's second-largest bauxite exporter in the long term. In Sierra Leone, the completion of Maforki Port in May 2025 marks a milestone in the country's bauxite exports. Following this, bauxite departures from the country reached a record high of 0.54 Mt in July, and are expected to surge to 5 Mt in the whole of 2025 and over 7 Mt in 2026. The country's total bauxite export capacity is on course to reach 8 Mtpa in 2025/2026 and double to 16 Mtpa by 2026/27 through successive expansion phases. Elsewhere in Western Africa, Cameroon is set to join the bauxite export landscape by Q1 2026. The country's first bauxite project, Minim Martap, developed by Canyon Resources, is expected to reach a production capacity of 6 Mtpa, with potential to scale up to 10 Mtpa in the longer term.

Heavy Chinese investments in the expansion of existing projects and new mines are expected to boost annual bauxite exports from Guinea to over 200 Mt in 2028/2029. Meanwhile, production expansion or new projects in Australia, Sierra Leone, Cameroon, and other emerging exporters such as Guyana and Ghana are anticipated to elevate the seaborne export capacity outside Guinea to over 90 Mtpa by 2029/2030, up from around 60 Mtpa in 2024. While these volumes are unlikely to displace Guinea's pre-eminent position in global trade, they may constrain its market share to around or below 70%, effectively curbing the potential for further dominance and diversifying global supply routes.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Transit activity through the Strait of Hormuz remained heavily suppressed (Link) Middle East Mayhem (Link) Strait of Hormuz Disruption - Scenario Analysis (Link) Dry 🚢 Dry Bulk Impact of Trump's Spain Threat (Link) Agricultural Freight Overview (Link) Other 🌎 The Supreme Court’s IEEPA tariff decision: What...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Russian Diesel Tanker Sails for Cuba as U.S. Order Blocks Oil Imports (Link) Does The Buy And Hold Strategy Still Work? (Link) Alaska Crude Diverts to Asian Markets (Link) Dry 🚢 A Market Increasingly Driven by Minerals Rather Than Energy (Link) Agricultural Freight Overview (Link) Other 🌎 Can Project Vault...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Reassessing Russian Supply (Link) Mainstream oil supplies return to normalcy as surplus falls (Link) Moscow, we have a problem (Link) Dry 🚢 Bauxite offers real positivity for capesizes (Link) Agricultural Freight Overview (Link) Copper Insights: The Supply-Demand Disconnect (Link) Other 🌎 How accurate were...