A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Iran Formally Closes the Strait of Hormuz 🇮🇷 Can the US Keep It Up? 🇺🇸 Tanker Midterms – 2026 Edition 🛢️

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

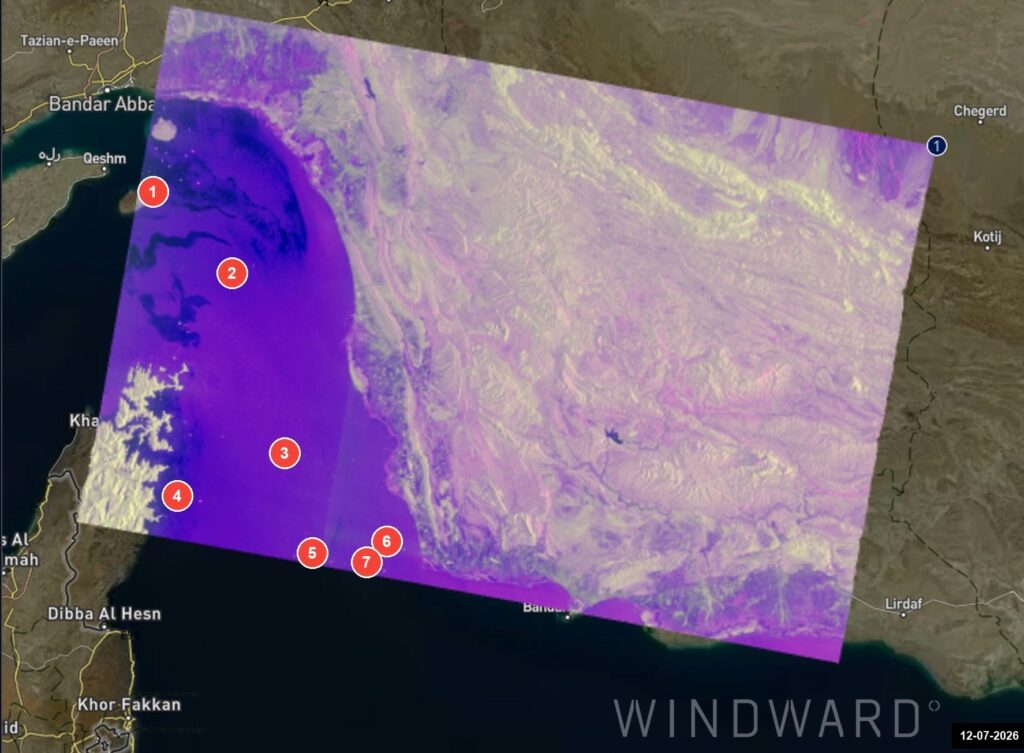

Iran Formally Closes the Strait of Hormuz as the U.S. Launches a Third Round of Strikes - WindwardIran has formally closed the Strait of Hormuz. The IRGC declared the waterway closed until further notice following its strike on a Cyprus-flagged container ship for using what it described as an unauthorized route, marking the first formal closure declaration of the conflict. The U.S. responded with a third round of strikes on July 11, hitting approximately 140 Iranian military targets. Iranian retaliation has now widened geographically to include Jordan, Qatar, Bahrain, and the UAE, with the IRGC targeting Prince Hassan Air Base in Jordan and air defenses activating across three Gulf states. Qatar’s Transport Ministry issued an urgent advisory suspending all maritime vessel activity until further notice, the first blanket maritime suspension by a Gulf state since the conflict began. The suspension has direct implications for LNG export flows from Ras Laffan. Iranian crude export volumes have not declined despite the escalation. What has changed is visibility and timing, with loadings spiking sharply on July 6 ahead of a feared return of the U.S. blockade before falling to near zero by July 9 to 11 as AIS transponder shutdowns spread across the sanctioned fleet. Nine OFAC-sanctioned National Iranian Tanker Company vessels have gone dark off Port Klang, Malaysia, carrying approximately 14.59 million barrels of Iranian crude and condensate, worth an estimated $989 million, bound for Shandong teapot refineries under the established Iran-to-Malaysian-blend-to-China laundering route. Iran Declares the Strait Closed After Striking a Cyprus-Flagged Container ShipThe IRGC struck a Cyprus-flagged container ship transiting the Strait of Hormuz on July 11, causing significant damage to the engine room, with one crew member reported missing. The IRGC attributed the strike to the vessel’s use of an unauthorized route. Following the strike, Iran declared the Strait of Hormuz closed until further notice. Iran launched retaliatory missile and drone strikes on U.S. bases, with the IRGC saying it targeted Prince Hassan Air Base in Jordan. UAE authorities said they were responding to missile and drone threats. Bahrain activated sirens and told residents to seek shelter. Qatar’s Ministry of Defense said it intercepted a missile attack targeting the country. The strike exchange has now widened geographically to include Jordan, Qatar, Bahrain, and the UAE. Oman has drafted a tentative proposal for managing routes in the Strait, while U.S. officials have stated that negotiations on nuclear weapons cannot progress until the Strait is secure.

Strait of Hormuz TransitsJuly 11 recorded 21 transits, nine inbound and 12 outbound, continuing the sharp downward trend documented across the reporting period. The inbound group comprised six AIS-transmitting and three dark vessels, with two tankers under Guyana and Hong Kong flags, two bulk carriers under Iran and San Marino flags, and two cargo vessels under Comoros flags. Six transited via the northern corridor with no southern corridor inbound traffic recorded. The outbound group comprised seven AIS-transmitting and five dark vessels, with three tankers under Mozambique, Liberia, and Netherlands Caribbean flags, one bulk carrier under the India flag, and four cargo vessels under Comoros, Bolivia, Netherlands Caribbean, and Iran flags. Seven transited via the northern corridor and one via the southern corridor. Windward assesses the near-total collapse of southern corridor usage, with one of 12 outbound vessels and zero inbound vessels, reflecting the sustained IRGC enforcement posture and continued operator avoidance of the Omani-side lane. Dark Vessel Consolidation Off the UAE and Oman CoastA ship-to-ship transfer pair was observed off the UAE and Oman coast, comprising two dark vessels of approximately 310 meters each with no AIS from either hull. Four additional dark vessels ranging from approximately 80 to 330 meters were assessed as moving inbound. One dark stationary vessel of approximately 140 meters was newly present in this collection with no detection in the prior pass, assessed as a possible new arrival. A probable dark container vessel of approximately 350 meters was transiting the same corridor.

Can the US Keep It Up? - GibsonsOver the course of more than 100 days of the Strait of Hormuz closure, the US proved to be the single most important source of replacement barrels, both for crude and clean products. The increase in US crude exports has been nothing short of spectacular: in the second quarter of the year, exports averaged around 5.2 mbd, up by 1.4 mbd compared to the 2025 average. The biggest growth was seen in long haul trade to Asia, which doubled from the 2025 baseline. Unquestionably, this growth was for the most part fuelled by the colossal US SPR release, helped by a modest increase in domestic US production. A similar trend was observed for clean exports, though increases here have been more modest. Total clean exports averaged close to 3 mbd in Q2, 450 kbd above their 2025 baseline, with the biggest gains in absolute terms seen in trade to Europe, Africa and Asia. With the ceasefire unravelling and attacks in the Strait resuming, exports from the Middle East Gulf are unlikely to recover anytime soon. The need for replacement barrels therefore remains significant but can the US continue to deliver at such elevated levels? Commercial crude stocks are notably down to their lowest level for this time of the year since 2018. An even bigger drop is seen in SPR levels, which nosedived, falling to 319.5 mbbls in early July, their lowest level since 1983. Still, inventories are down by just 96 mbbls from late February (although 133 mbbls have been awarded), compared to the 172 mbbls announced in March, meaning more barrels are still to come, though it is unclear what will happen to the 39.5 mbbls not sold in the latest tender. Beyond that, further releases appear less likely, with growing concerns about the minimum SPR level needed to maintain functionality and the industry warning the reserve must stay at least 20% full (roughly 143 mbbls) for operational reasons. In any case, with domestic refining runs extremely elevated, US refiners could absorb much of the remaining release, limiting the volumes reaching the export market. Preliminary AIS data shows that weekly USG crude exports have been in steady decline since late May, falling last week to their lowest level in three months. On the upside, US crude production is edging up, with the latest estimates from the EIA pointing to an increase of 200 kbd this year and a further 250 kbd in 2027. Projections have been revised up in recent months amid higher oil prices and hedging by producers. The rig count is also responding, up more than 40 units year on year after eight consecutive weekly gains. With geopolitical tensions escalating once again, and upward pressure on oil prices reemerging, further upward revisions to US crude output may also be on the cards. Nonetheless, rising production cannot fully offset the loss of SPR barrels once the current release programme runs its course.

Tanker Midterms – 2026 Edition - Poten & PartnersTop Reported Dirty Spot Charterers for 1H 2026* The first six months of 2026 are behind us and the conflict in the Middle East has dominated the headlines globally. It has also had a profound impact on the oil and tanker markets, as reflected in this review of the reported spot activity. Effectively removing the Arabian Gulf from the tanker spot market for four months has dented fixture volumes. Compared to the same period of last year, the reported total cargo volumes in H1 2026 declined by 21 million tons (3.6%), while the total number of reported spot fixtures was down by 5.7%. China significantly reduced its crude oil imports in the aftermath of the conflict in the Middle East. That shows in the VLCC spot fixture count. While Unipec remains the top VLCC charterer, with 217 reported fixtures, it is a 32% decline from the 317 fixtures we recorded last year. In contrast, Petrobras solidified its second place, increasing its fixture count from 52 in H1 2025 to 73 this year (+40%) reflecting Brazil’s growing crude oil exports. Overall, the number of reported VLCC spot fixtures declined from 1,447 in H1 2025 to 1,385 this year. In H1 2026, the Suezmax segment was dominated by the traditional oil majors, with Chevron, Total, ExxonMobil, BP and Shell making up the top 5. Suezmax volumes were less impacted by the closure of the Strait of Hormuz. The number of fixtures declined by 2%, from 855 in H1 2025 to 841 this year.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Trumping 2025 (Link) Jones Act Vessels For International Crude Trade (Link) Full Steam Ahead? Not So Fast! (Link) Dry 🚢 Iron Ore Surplus Builds as Chinese Steel Margins Remain Under Pressure (Link) Weekly Grains & Oilseeds Outlook -26/06 (Link) China’s coal imports in May fell 8% year-on-year (Link) Other 🌎...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Oman’s Offshore Oil Trade (Link) Has The US Flipped The Script? (Link) Strait of Hormuz in April: A Stop-Start Recovery Under Persistent Risk (Link) Dry 🚢 South Asian demand keeps pushing coal flows higher (Link) Agri - Freight Recap: 12/06/2026 (Link) China Mineral Resources Group has reportedly told some...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Import loss, stock build: How China absorbs the Hormuz shock (Link) From Supply Disruption to Transit Disruption: What April Reveals About the Global LNG Shock (Link) OFAC’s Crackdown on Chinese Teapot Refineries (Link) Dry 🚢 China’s soybean imports in March rose 14.9% (Link) Agri- Commodities: 27-01/05/26...