A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Port Fee Saga 💵 What lies ahead for Russian oil exports? 🛢️ A New VLCC Leader - Inside Sinokor’s Market Rise 🚢

|

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Other 🌎

Port Fee Saga - GibsonsIt is likely that many people in the shipping industry were hoping we had seen the last of additional port tariffs in October, after the US Trade Representative’s (USTR) Section 301 tariffs targeting Chinese owned, operated or built ships were put on hold for a year, with China also lifting its own retaliatory measures. However, after causing havoc in 2025, the port fee saga has its latest instalment. On Friday the 13th of February, the Trump administration published their most recent plan to restore America’s maritime dominance. The plan contains incentives for fleet expansion of US built, US flagged vessels, by subsidising the modernisation of shipyards, including new drydocks, aimed at increasing throughput and decreasing construction timelines. Further, whilst these measures are carried out, the proposal contains a provision to bring foreign-built vessels under the US flag to carry international trade in the interim. The funding required is intended to come from the Maritime Security Trust Fund, which in-turn will derive its income from the latest plan for US port fees. Details remain thin, but the plan proposes a fee on all foreign-built commercial vessels entering U.S. ports, with costs based on the weight of imported cargoes, set at between $0.01-$0.25 per kg. Only about 1% of tankers above 25,000 DWT are US built, which means this plan would cover virtually all tankers. At the lower end of the range, at $0.01 per kg, the fees would imply a cost of around $2.7m per voyage for a fully laden VLCC discharging into the US, or around $450,000 on a fully laden MR. At the upper end of the range, at $0.25 per kg, the fees would reach a cost of around $68m per voyage for a fully laden VLCC discharging into the US, or around $11m on a fully laden MR. These costs are even steeper than those in the previous plan, and even at the lower end of the range would be prohibitively expensive. Vessels arriving in ballast would be exempt, yet contrary to previous iterations of US port fees, no details for any further exemptions are currently included in the plans. Notably, the latest proposal applies to all foreign-built vessels and is not China focused, levelling the playing field. Considering the US Trade Representative’s (USTR) Section 301 tariffs were postponed shortly after being implemented, when China rapidly implemented significant retaliatory fees, these latest port fees seem unlikely to be enacted in their current version. It is also unclear whether the latest plans will replace the earlier regime. The proposal appears to be in its infancy, with few details and no implementation framework in place. Further, congressional approval is likely required for this plan to be enacted, which presents a considerable hurdle. One thing is clear, the latest details of Trump’s Maritime Action Plan signal continued intent from the Trump administration to revive the American shipping industry. Whether the plans improve the competitiveness of US shipyards remain to be seen. Currently, the costs of constructing virtually any type of commercial vessel remain significantly higher than at competing Korean, Japanese, or Chinese shipyards, and capacity significantly lower.

What lies ahead for Russian oil exports? - VortexaIn the wake of October 2025 Lukoil and Rosneft sanctions, Russia’s oil supply chain has come under increasing strains. December 2025 – January 2026 seaborne crude oil exports out of Russia (ex. CPC, KEBCO) averaged nearly 500kbd above the call for arrivals, following a robust export program amid growing compliance risk.On a seasonal basis, the difference in Russia’s seaborne crude exports between December 2025 (dataset seasonal maximum) and December 2022 (respective minimum) is +1.1mbd. The two periods bear contextual similarity - the EU ban on Russian crude imports (Dec-2022) and the deadline to phase out imports from newly sanctioned producers (following in Dec-2025).A notable differentiating factor, which underpinned sustained seaborne export programme in late 2025 despite tighter sanctions, was Russia’s established trade relationship with the East - India and China.However, Russia’s ability to maintain strong crude exports may come into question if India further pivots away from Russian grades under the India-US trade talks.

While India reconsiders, China remains a steady buyer of Russian crudeThe share of Russian oil in India’s total crude imports has been on a downward revision since last December, falling to 20% this February (~1.1mbd, days 1-24), compared to 36% in November 2025. Amid India-US trade negotiations, only the EU-sanctioned Nayara refinery continues a robust import program of Russian crude.In contrast, share of Russian oil in China’s total seaborne crude imports rose to 18% in February, reflective of ~1.9mbd (days 1-24), compared to 11% last November. Nearly 90% of incoming Russian volumes were delivered into Shandong and fully absorbed by private refiners, as state-owned Sinopec has pulled back from Russian purchases since November. This marks a dataset high in arrivals of Russian crude into the province, supporting the climb of Shandong onshore crude inventories to ~367mb to date, reflecting 54% tank utilisation.Private inventories retain sufficient flexibility to absorb extra barrels, even as the majority of China’s expected new storage capacity is state-owned and would favour mainstream crude.

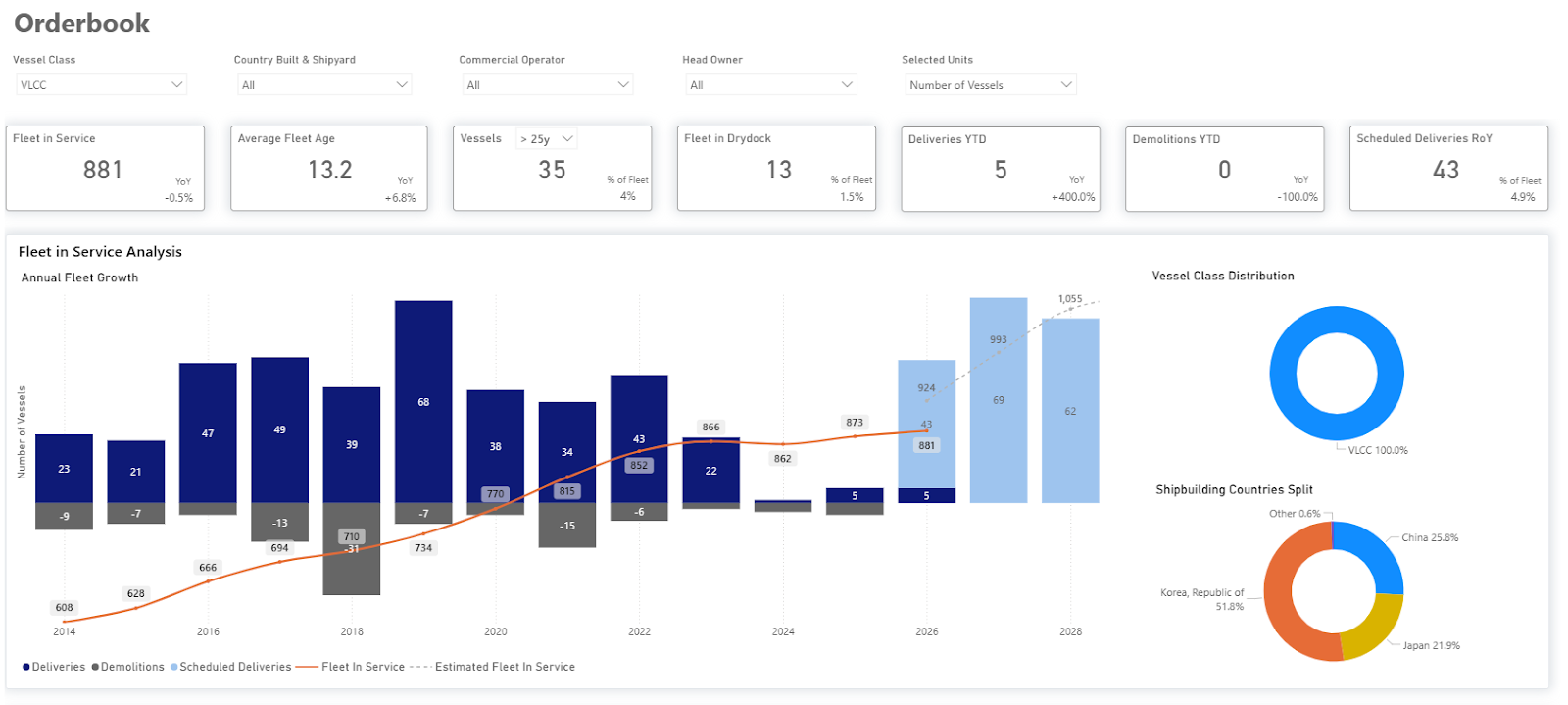

A New VLCC Leader - Inside Sinokor’s Market Rise - Signal OceanGlobal VLCC fleet capacity is projected to expand more aggressively through 2028. Taken together, scheduled deliveries from all major shipbuilding countries imply an average annual VLCC fleet growth rate of approximately 6% by 2028, assuming the current orderbook is delivered as planned.

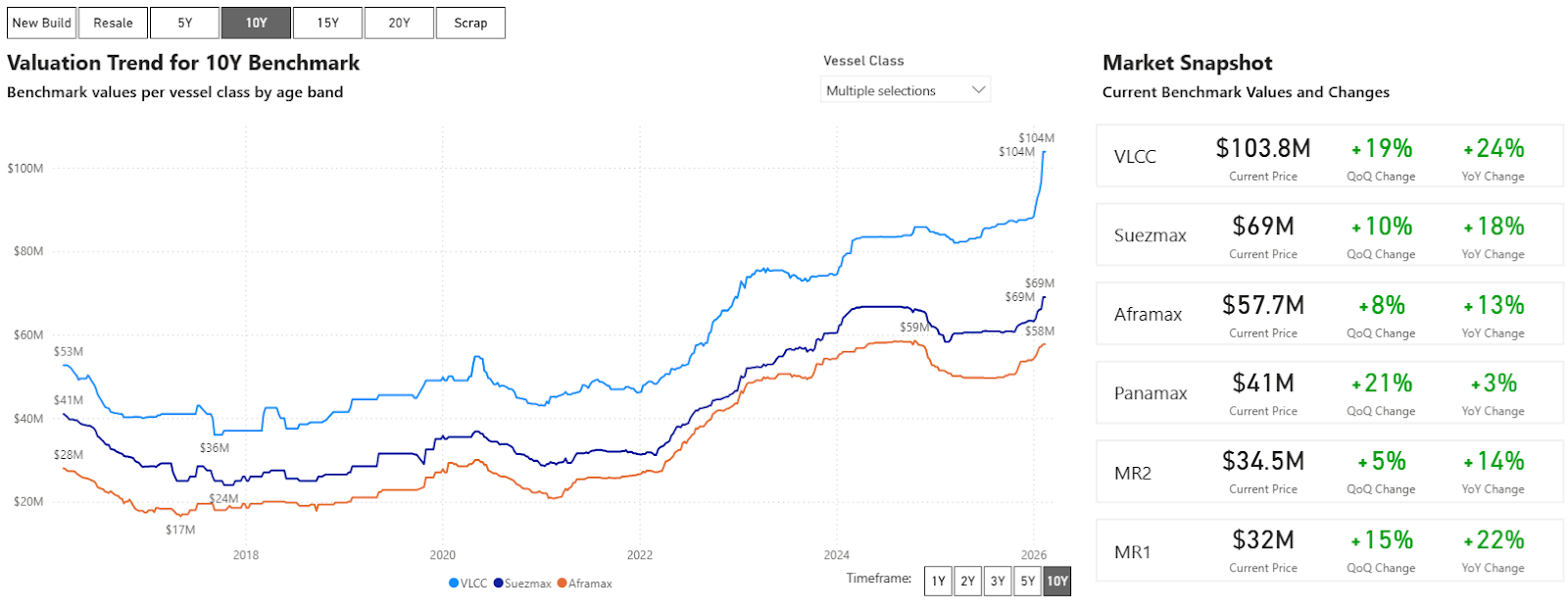

Within this evolving environment, Sinokor Merchant Marine (Sinokor) has expanded its VLCC commercial footprint, positioning itself as the single largest Commercial Operator in terms of fleet size. The company’s timing aligns with a transitional point in the tanker cycle, where the balance between vessel supply growth and effective transportation demand will influence freight rate direction. Data derived from the Signal Ocean Platform (TSOP) were used to evaluate the impact of Sinokor’s expansion on the VLCC market. The analysis examines fleet size, market share, and age distribution in order to provide a comprehensive and data-driven assessment of how Sinokor’s positioning alters the competitive landscape. Sinokor’s Strategic ExpansionOver the past few months, it has been widely reported that Sinokor has embarked on an aggressive expansion in the VLCC segment, targeting both secondhand acquisitions and time-charter arrangements. Market chatter intensified in mid-December, pointing to a notable uptick in tanker S&P activity, although transaction details and counterparties were not yet fully disclosed. By January, greater clarity began to emerge, with Sinokor identified as the principal buyer behind a substantial number of VLCC transactions. Reported figures varied considerably, with market estimates ranging from 20 to as many as 50 units. As of today, we have confirmed 36 acquisitions through cross-referencing multiple market reports with TSOP vessel lists, which indicate Sinokor as the new Commercial Operator in the majority of cases. Approximately 26 vessels have already been delivered, while a further 10 are scheduled for delivery within the current or early next quarter. This total may increase further as additional transactions are finalized and pending deliveries are completed. The aggressive expansion of the VLCC fleet is noteworthy, as the decision coincides with an upward trend in benchmark valuation assessments. For instance, the valuation for a 10-year-old VLCC has experienced a 24% annual increase, reaching its highest value in the last decade.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai +44 (0)208 050 9806 You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ How much of China's crude demand will return? (Link) "El Niño" Declaration Pressures US Crude Export Outlook (Link) Why China’s Crude Collapse Isn’t The Demand Story It Looks Like (Link) Dry 🚢 Q2 Sees Global Met and Thermal Coal Flows Accelerate (Link) Freight Outlook - 10/07 (Link) Frances Maize Crop Drops...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Trumping 2025 (Link) Jones Act Vessels For International Crude Trade (Link) Full Steam Ahead? Not So Fast! (Link) Dry 🚢 Iron Ore Surplus Builds as Chinese Steel Margins Remain Under Pressure (Link) Weekly Grains & Oilseeds Outlook -26/06 (Link) China’s coal imports in May fell 8% year-on-year (Link) Other 🌎...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Oman’s Offshore Oil Trade (Link) Has The US Flipped The Script? (Link) Strait of Hormuz in April: A Stop-Start Recovery Under Persistent Risk (Link) Dry 🚢 South Asian demand keeps pushing coal flows higher (Link) Agri - Freight Recap: 12/06/2026 (Link) China Mineral Resources Group has reportedly told some...