A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

US tariff threat looms over crude and refined product flows 🛢️ Trade Lane Review: Far East - East Coast North America 🌎 India's Aluminium Boom Leading Rising Bauxite Imports 🇮🇳

|

Maritimedata.ai is a digital broker of data and analytics solutions for the maritime ecosystem. Source, Evaluate and Purchase maritime data and analytics from the largest network of specialised providers in the world. 200+ Products 50+ Maritime Intelligence Providers 30+ Years of Experience Insights 📈Oil & Gas 🛢️

Dry 🚢

Explore, test, and feedback on maritime data solutions before they hit the market.We're delighted to be launching a number of beta tests for new-to-market data services over the next few months, and we'd like to offer you the opportunity to take part. Upcoming Opportunities 2025

How to get involved?You can register your interest for future beta tests below.

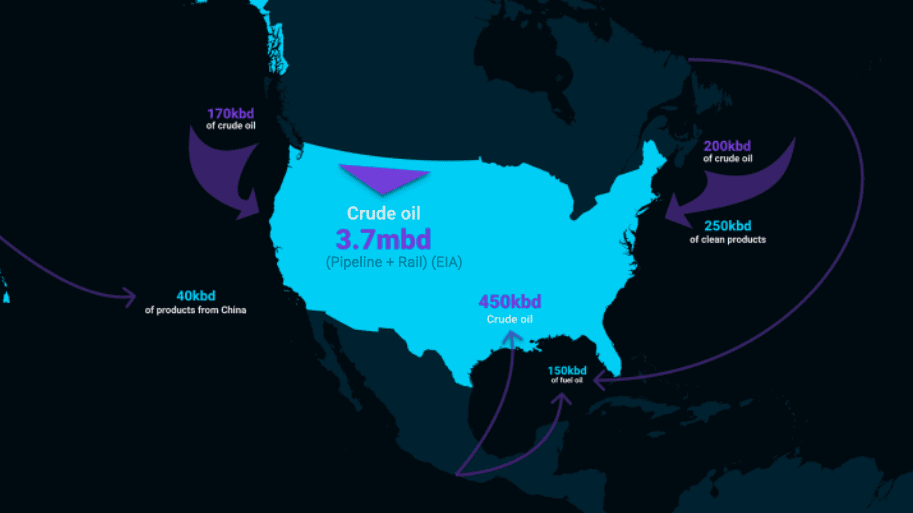

US tariff threat looms over crude and refined product flows - VortexaPresident Trump’s proposed tariffs on Mexican and Canadian energy imports have been delayed for now until early March, but the uncertainty around their eventual implementation still persists in the markets. The story so far is that these potential tariffs on Canada and Mexico could severely limit the choices for US refiners forcing them to look for alternatives and some might find it difficult to run their refineries optimally. US Midwest refiners, who rely mainly on Canadian crude via pipeline, might see a reduction in run rates and challenging economics if tariffs are imposed. Tariffs on Mexican crude imports could also deprive several USGC refiners of heavy grades that may not be easily replaced. The recent announcement of 25% steel and aluminium tariffs beginning March 12 has only heightened ongoing uncertainty.

What is at stake?The largest flow that could be impacted is the ~4mbd (Jan-Nov 2024 avg. from EIA data) of crude oil imports from Canada to the US. Of these 3.7mbd are land based, mainly pipeline and some rail volumes with the remaining volumes being seaborne. According to Vortexa data for Q4 2024, around 170kbd of Canadian crude made its way into the US West Coast from Vancouver via water, these being the TMX pipeline barrels which could be redirected to Northeast Asia in face of tariffs. There are also some 200kbd of crude flows from East Coast Canada which could also be impacted. Similarly there are also 250kbd of clean product imports into US PADD 1/Atlantic Coast from EC Canada which would require redirection elsewhere. The next biggest flow is 450kbd of seaborne imports of Mexican crude, mainly into the US Gulf Coast which would be of utmost concern to USGC refiners and will have them scrambling for replacement barrels if tariffs are put in. The US also imports some ~100kbd of residual fuel from Mexico and another 50kbd from EC Canada which will potentially be impacted. Finally there are small volumes of around ~40kbd of clean products that are imported from China which could be impacted. We shall discuss more about US-China energy flows in the next section. Chinese tariffs already in effect

As US applied tariffs on Chinese imports came into effect on February 4, China announced its own counter-tariffs on US energy imports including crude, LNG, and thermal/coking coal which took effect on February 10. The retaliatory tariffs on US energy imports include 10% and 15% import tariffs on US crude and LNG respectively; however we maintain that the impacts will be minimal given flows constitute 5% or less of China’s total imports and the US originated cargoes can be easily redirected to other destinations in Asia. China chose not to put tariffs on US LPG and ethane imports, which constitute the main energy flow between the two countries.

Trade Lane Review: Far East - East Coast North America - eeSeaWe kick off this analysis with the knowledge that many service versions have already begun, but it will still be a couple of weeks before many of these maiden voyages on Gemini Cooperation and Premier Alliance services reach their first ports of discharge on the Northern European and Mediterranean shores.

Trade capacity evolution during transitionsTwo major factors that contribute to the proforma capacity slump observed in February on all E/W trades are the alignment between the early Lunar New Year and alliance transitions, and the fact that there is no hard cut-off for end/start dates across old and new alliance services. This means that there are long periods of lull in planned sailings where a service like The Alliance’s MD3 will have sailings into its first port of discharge suspended by week 10, but arrivals on Premier Alliance’s MD3 are not planned to arrive until week 14. This is not taking into account any actual delays that would be accrued and built into live forecasts along the way. Alliance transitions coinciding with the Lunar New Year mean that while blank sailings are used for both strategic purposes like offsetting delays on first voyages, they also allow carriers to suspend some services ‘early’ instead of inserting blanks as they usually would in the corresponding holiday weeks in January or February. You can read more about this phenomenon and its impact on capacity in the Far East - West Coast North America analysis, our analysis of the PMR - PS3, or in the recent article by our friends at Journal of Commerce.

India's Aluminium Boom Leading Rising Bauxite Imports - AXSMarineIndia’s aluminium sector is undergoing a notable shift with domestic producers increasingly depending on imported Bauxite to satisfy growing demand. In 2023, bauxite imports exceeded 3.7m MT, representing a 6.3% year-over-year increase. This momentum continued into 2024, with an additional 20% increase to over 4.5m MT, signalling the industry’s deepening reliance on external sources to fuel its accelerating expansion. The majority of this demand stems from the flourishing domestic market, valued at $11.28bn in 2023 and predicted to reach $18.84bn by 2030 — a projected 7.6% compound annual growth rate. Aluminium consumption is being propelled by vital sectors such as construction, automotive, and electronics. Construction, in particular, has embraced aluminium’s lightweight yet durable characteristics, incorporating it into modern infrastructure projects.

Despite India being as the world’s second-largest aluminium producer, local Bauxite extraction has not managed to keep pace with industry requirements. Environmental regulations, complex land acquisition processes, and organized resistance from local communities have slowed domestic mining expansion. Additionally, certain Bauxite deposits in India contain higher impurity levels, raising costs and reducing efficiency when converting bauxite into alumina. In response, Indian companies are pouring resources into large-scale alumina refining ventures that hinge on a stable bauxite supply. Hindalco Industries recently announced between $4bn and $5bn investments for expanding its aluminium and copper production capacities, while Vedanta Aluminium boosted the annual refining capacity at its Lanjigarh facility from 2m tonnes to 3.5m tonnes, with a roadmap to reach 5m. These upgrades underscore the necessity for continued - or in many cases, increased - Bauxite imports.

How we can help:

Thank you for your time. Regards, James Littlejohn Co-Founder Info@maritimedata.ai You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologise for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe. |

Maritime Data Newsletter

A dedicated source of market insights and product developments from the largest network of specialised providers of maritime data and analytics.

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Transit activity through the Strait of Hormuz remained heavily suppressed (Link) Middle East Mayhem (Link) Strait of Hormuz Disruption - Scenario Analysis (Link) Dry 🚢 Dry Bulk Impact of Trump's Spain Threat (Link) Agricultural Freight Overview (Link) Other 🌎 The Supreme Court’s IEEPA tariff decision: What...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Russian Diesel Tanker Sails for Cuba as U.S. Order Blocks Oil Imports (Link) Does The Buy And Hold Strategy Still Work? (Link) Alaska Crude Diverts to Asian Markets (Link) Dry 🚢 A Market Increasingly Driven by Minerals Rather Than Energy (Link) Agricultural Freight Overview (Link) Other 🌎 Can Project Vault...

Maritimedata.ai is a single source of access to 200+ data services. 200+ Products 60+ Maritime Intelligence Providers 30+ Years of Experience Explore our catalogue Insights 📈 Oil & Gas 🛢️ Reassessing Russian Supply (Link) Mainstream oil supplies return to normalcy as surplus falls (Link) Moscow, we have a problem (Link) Dry 🚢 Bauxite offers real positivity for capesizes (Link) Agricultural Freight Overview (Link) Copper Insights: The Supply-Demand Disconnect (Link) Other 🌎 How accurate were...